DInvests half year review.

2025

As we’ve crossed the half way point during the 2025 investment year. I thought it would be beneficial to look through my portfolio of performance, buys and sells, books and content I’ve read and any mistakes made and share it with my subscribers.

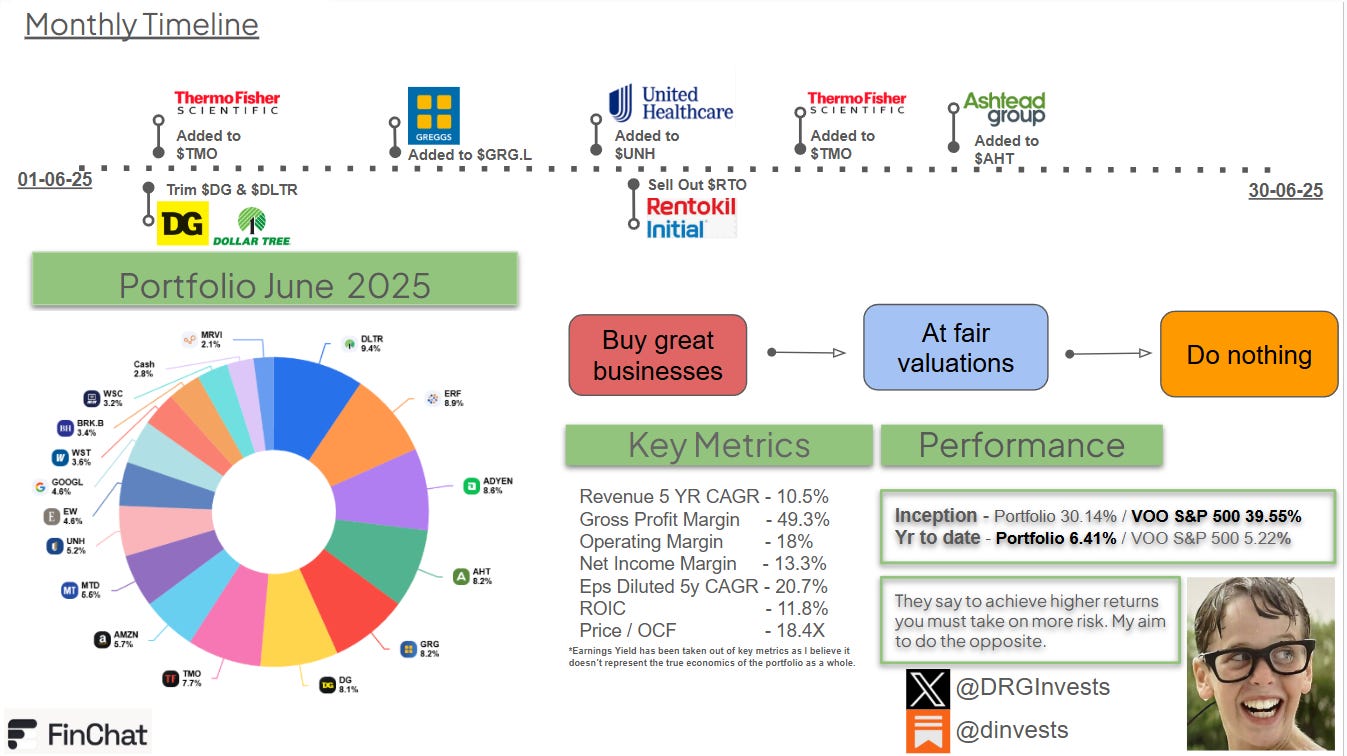

Here’s the DInvests portfolio at the end of June 2025 as recently posted during my monthly update. If you’ve missed this update you can access it here.

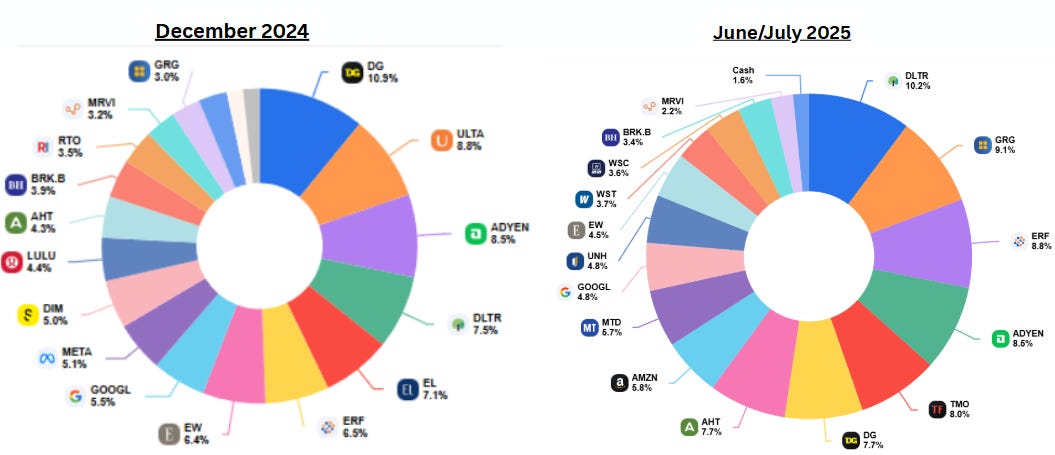

Before I dive into the pathway that’s constructed the portfolio to what it looks like today, I’ll compare the portfolio from my December 2024 update.

A total of seven businesses have left the portfolio which, without taking weight as a factor represents a total of a 36% stock turnover which is way more than I initially planned. Looking into 2026, depending on no story changes within the businesses I own, I plan to reduce this metric dramatically. I can honestly say I believe the portfolio today outweighs the former with quality, growth prospects and their competitive positioning all while purchasing them at very reasonable, even cheap valuations.

Businesses Sold

Estee Lauder 💄- This sale wasn’t easy and resulted in my largest loss as an investor 😒. Initially purchased as a turnaround bet, Estee Lauder, which is still operated by the Lauder Family is a world leader in skin care and beauty products with 70-80% gross margins. The initial thesis was a return to normalised operating margins after issues in their Asia travel retail business to resolve within 12-18 months. This wasn’t the case. Their profitability was also heavily dependant on their skin care segment with China being their largest market. I can put my hands up here and admit I was wrong with regards to their competitive positioning.

Ulta Beauty 💄- Ulta was another heavy weighted position in the start of January and was sold at the end of May for a small gain. Nothing changed here regarding my thoughts on the business but more attractive businesses surfaced. Thermo Fisher and United Health was purchased.

Lululemon 🏃♀️- More of a short term play. I’m very familiar with the brand and love their products but retail is a tough industry, Purchased the stock during the lows it reached in May 2024 and sold after a rise in price for a decent realised gain.

Sartorius Stedim 🔬 - One of my more expensive businesses which offered the lowest IRR at the time with which it was sold. I added Amazon at $170 dollars with the proceeds, a very reasonable price for such an amazing business which has been on my radar for a while. As I was fully invested during this time, funds needed to be available and DIM 0.00%↑ was the unlucky culprit.

Core and Main 💦 - Core and Main CNM 0.00%↑ was sold purely to fund my new West Pharmaceutical investment. I still believe CNM to be a high quality business but WST possesses better all round quality fundamentals. The switch was relatively easy to justify as CNM has low barriers to entry, their products are commoditized and the industry is cyclical being tied to the health of the economy. The qualities of these two are widely separated.

Rentokil 🐀 - An excellent business with stable end markets and recurring revenues, however, there’s still some tangible headwinds within its operations in the US with regards to the integration of their large Terminix acquisition. The near future for the business still looks challenging and I used this opportunity to sell and add more funds into Thermo Fisher.

Meta 📱 - I’m not bearish on Meta. Quite the opposite. Sold at $680 back in January at a earnings multiple of 30x and a FCF multiple ex SBC of 47X. As I mentioned in my update in January, I believe for superior stock performance in the future the business would have no room for error and the margin of safety was diminished. With a 600% gain from my buy price after aggressively buying in the low $100 and sub $100 I captured most of the excess returns in the stock.

Summary

Looking back at the businesses I exited in the first half of the year, I can truly say only one (Estee Lauder) was sold due to a mistake. All other sales where purely to fund better opportunities I believed the market presented to me. United Health, Mettler Toledo, Thermo Fisher, Amazon being stand out names in this regard with also additions to Greggs, Dollar Tree and Eurofins scientific who’ve all grown to a meaningful portion of the portfolio. Where these the right choices? Time will tell.

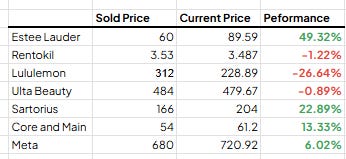

Looking into the performances of the businesses sold.

Out of the seven businesses sold, three have declined with four gaining some ground. Ironically, the leader here, Estee Lauder which is up 49% since I sold. However, this doesn’t change the fact that the business is highly dependant on one segment for their profitability (Skin care) and also highly reliant on the Asia market. True, these where tangible when I entered the position but I misinterpreted how important they where to the business. Throw in some overpriced poor acquisitions which has resulted in impairment charges and massive changes to the management team I still believe my decision to exit the stock was the correct one.

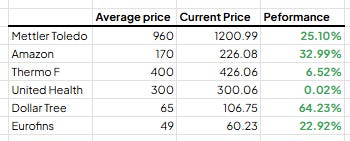

I’ll proceed here showing you the stocks I purchased during the same timeframes.

I know investment decisions, whether successful or unsuccessful in such a short time frame of six months shouldn’t be based on stock performance. I honestly take the stock performances posted above with a grain of salt and I’m not anchoring on these for successful conclusion on stock picking. Even if all my substitutions where in the red, it wouldn’t bother me the slightest as I know they are all high quality companies and in the long run should produce acceptable returns.

Businesses Purchased

As many of my subscribers know, I regularly publish reports on stocks I’ve added. Below, will be a brief description of each with links to dedicated articles on the business.

Mettler Toledo - MTD is an industry leader in laboratory balances, pipettes, titrators and reactors among other lab equipment instruments along with their integrated software solutions LabX. They have products in each stage of their customers workflow from R&D research, quality control, scale and production, filling, logistics and packaging. With excellent economics, strong ROIC and resilient end markets that promises good long term growth, MTD was a quality business at a reasonable price.

Amazon - Amazon needs no introduction. After missing out on Amazon sub $100 back in 2022 its been on my radar ever since. Even though my purchase price was 70% higher than when I could have pulled the trigger in 2022, on a P/OCF (a preferable metric when analysing Amazon) it’s actually the lowest its been in the past 10 years. Again, a very high quality business that’s renowned as an innovator and disruptor. Who knows where Amazon will be 10 years from now, I can confidently guess it will be much larger with new revenue streams even the most intelligent investors will not have calculated into its valuation. As a regular Amazon customer I know first hand the value they bring to their customers. I’m happy its in the portfolio….. and for the long term.

Thermo Fisher - ThermoFisher is a life science and clinical research company. It’s a global supplier of analytical instruments, clinical development solutions, specialty diagnostics, laboratory, pharmaceutical and biotechnology services with leading positions in all their reporting segments. Secular tailwinds, recurring revenues protected by high regulatory barriers and resilient end markets shields TMOs revenues and offers good insight into predictable future revenues. After a 30% sell off in share price presented a good risk/reward bet.

United Health - Purchased sub $300 after a 50% drop in share price after higher than expected utilisation (costs) in their Medicare advantage plans, management changes, withdrawing earnings guidance and rumours of criminal investigations imminent. After denying all accusations, their old CEO Stephen Hemsley who has 11 years of past leadership tenure at UNH, the dynamics of short tail health insurance plans that can be repriced in the near term along with their scale I believe this sell off was severe. At an EV/EBIT of 9.8x for the largest health insurer in the United states was too good to turn down.

Dollar Tree - Continued to add into my existing position which has been reaping rewards as of late. My basket approach between Dollar Tree and Dollar General is paying off after buying at dirt cheap valuations. The earning power of these businesses are remarkable and resilient through all economic conditions. After its divestiture of Family Dollar, Dollar Tree can now focus solely on is higher margin business.

Eurofins - Continued conviction in the mid 40’s makes Eurofins a number three holding as of writing. The most recent earnings and full year report show great progress in the business with strong revenue growth and also progress in the companies growth and efficiency goals. (Start ups, Investments in owned sites, Acquisitions at attractive valuations and continued investments in their integrated IT solutions). Buybacks have started to slow as the price has increased to 60 Euros. Industry tailwinds in the testing market make Eurofins a key long term holding.

Greggs - All I can say is I wish for a really cold summer 🫠……… Sales expectations were lower than anticipated in the most recent prelim results, however, like for like growth in company stores continued to stay positive. Greggs currently has a market cap of £1.8 billion, zero debt (Only leases), they produce £310 million in operating cash flow (LTM) and offer a dividend yield of 3.6%. My conviction here keeps growing as time passes and I can say Greggs is my number 1 position in my portfolio with regards to cash invested. Currently in the middle of a large investment cycle which is depressing free cash flow which they are using to build out new stores and their supply chain capacity, I believe once this phase ends cash flow will increase dramatically which should be reflected in the share price.

Summary

After being patient and waiting for excellent companies to become good value or even cheap. I can truly say that I believe decisions made during the first six months of 2025 strengthened the portfolio in terms of Competitive positioning, management, earning power, resilience and future growth prospects. Portfolio turnover going forward should be materially lower than the past.

Investing is a long practice and I’m still learning 📖. After 5 years of investing there’s still many things that I need to learn and master. One thing I have learned and I hope this resonates with my readers is that when a fat pitch arrives it shouldn’t take a complicated DCF model to justify its purchase, it usually only takes a “back of the napkin” valuation. This has been the case in my experience. Will my activity in the 1H yield good results?

Performance

Year to date the DInvests portfolio is up 8.6% compared to the Index which is up 6.8%. The main contributors have been my large allocation in the two dollar stores (Combined near 20%), Eurofins and Ashtead Group. The biggest detractor is Greggs which I’m taking full advantage and now sits second in weight.

Since inception the portfolio is up 30% compared to the Index of 41%. Here, the underperformance comes from a continued rising stock market with little weight in the Mag 7 of which the index combining all seven represent roughly 34% and also currency fluctuations which has had a negative affect on overall returns. Since I’ve been thoroughly keeping records and tracking my portfolio since 2022 to 2025 I’ve beaten the market two out of three years and am currently on track to beat it in 2025.

I’m confident during times of economic uncertainty, my portfolio will perform a lot better than the high flying index and over the long term will produce market beating returns.

Investment content

Investment material read during the year include only two books (Reason for the low count is due to more time researching companies), a handful of investment letters and many annual reports.

The two books read so far during 2025 and current. Links to the books are in the titles.

Currently reading “ Buffett and Munger unscripted” by TSOH Investment Research

All three are excellent investment books and I highly recommend.

The investors I follow and read their investment letters annually are Francois Rochon, Chris Bloomstran, Warren Buffett, Terry Smith and Tom Gayner. Links to each below.

Also, lets not forget the excellent investors here on Substack. Below is a list of some excellent accounts that provide excellent content.

If you don’t already, give these accounts a follow.

Thankyou for taking the time to read my half year review.

DInvests

DRGInvests on X

Disclaimer: I have a long position in all stocks mentioned in this article. I can’t guarantee the accuracy of the information provided in the newsletter. All statements express personal opinions and information gathered online. Any estimates, forward looking statements and assumptions made in this newsletter are unreliable. Do your own research. Any information in this newsletter is for educational and entertainment use only and should not be taken as investment advice.

Thanks for the shoutout, really great write-ups and performance. Keep it up!

Thank you for the shoutout man I appreciate it. You're smashing it!