"The PEG Ratio" Why its flawed.

A popular metric used by investors and famously implemented by Peter Lynch is the PEG Ratio. This ratio essentially compares the companies current P/E ratio with their expected growth rate. In theory, a lower PEG ratio is meant to indicate undervaluation with the opposite being true for overvaluation. I see many investors use this ratio to determine whether a company is cheap or expensive without any real in-depth analysis.

The PEG ratio has its flaws and one should consider these flaws when analysing or comparing businesses.

Here’s the formula,

PEG Ratio = P/E ratio / Expected growth rate in EPS

Reasons to be cautious taking the PEG ratio at face value.

The P/E ratio is derived from using “Share price / GAAP earnings per share” which takes into account any unusual and irregular gains and losses. Example, GAAP earnings include one-time events like restructuring charges, write-downs, and gains on sales, which can significantly impact earnings positively or negatively in the period.

Without careful analysis from the investor, a companies P/E ratio could be extremely low or extremely high due to these GAAP adjustments but will have zero reflection on the companies real operating performance. Here the investor will have to try and figure out a normalised level of operating performance adjusting any irregular gains or losses to compute a true earnings number which will give a true earnings ratio.

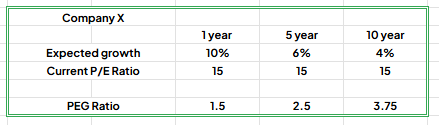

How long is the expected growth rate? Is it over 1 year? 5 years or 10 years? The choice of time horizon has a huge difference in the companies PEG ratio as shown in my example below. The 2% difference in growth rate in years 5 and 10 increases the PEG ratio by 50%. Also, a company with an extremely high growth rate in year one might look cheap on a PEG ratio basis only to look expensive in years 5 and 10 when growth eventually slows

The biggest problem with the PEG ratio when using for valuation purposes is the zero accountability of a companies ROIC which is arguably the most important driver of value creation and a sign of a companies competitive advantage.

In the image below two companies X and Y have the same P/E ratio of 17x with different growth rates of 5% and 10% resulting in a PEG ratio for company X of 3.4x and a PEG ratio for company Y of 1.7x. In this scenario we would assume company Y would be the better buy for the higher growth and lower PEG. However, this is before taking into account a companies ROIC.

4. Taking into account a companies ROIC we have to work out the companies NOPAT. For the purpose of this example both companies have zero debt resulting in zero interest so NOPAT should equal earnings.

Using a DCF model with the terminal value formula at the end of the forecast period with a 30% ROIC on the lower growth company of 5% and 14% ROIC for the 10% growth company we end up with equal values for both companies. Both companies have a terminal growth of 3% and a WACC of 9%.

The results show both companies trade trade at the same valuation of $19.9Bn. The reason for this is due to the following.

Company Y must reinvest more of its profits to grow. For growth of 10% with a ROIC of 14% the company would have to reinvest 71% of profits compared to 16% reinvestment for company X which has ROIC of 30% resulting in a 5% growth.

Growth = Reinvestment rate * ROIC

14% * 71% = 10%

30% * 16% = 5%

Lower ROIC results in higher reinvestment of profits for a desired growth rate resulting in less cash for investors.

Higher ROIC requires lower reinvestment resulting in more cash to investors.

As we’ve all been taught, a companies valuation is the available cash that can be taken out of the businesses at a reasonable discount rate from now until judgement day. ROIC is and always will be a factor in valuation. PEG doesn’t take it into account.

Conclusion

This article was not meant to deter investors away from using the PEG ratio but more of a case study for investors to dive deeper. A lower PEG ratio doesn’t mean a company is cheap or expensive as shown in the example above. The only possible way in my opinion to use this ratio and put to good use is two compare companies with the same financial and operating performance as the subject. Other than that I believe its a poor metric for valuation purposes.

Thank for reading

DInvests

DRGInvests on X.

Disclaimer: I can’t guarantee the accuracy of the information provided in the newsletter. All statements express personal opinions and information gathered online. Any estimates, forward looking statements and assumptions made in this newsletter are unreliable. Do your own research. Any information in this newsletter is for educational and entertainment use only and should not be taken as investment advice.