Nomad Foods - The Yield Machine

A 6.8% Dividend with Heavy Repurchases in a Low-Growth Era.

Overview

Name - Nomad Foods Ltd

Ticker - NOMD

Market cap - $1.44Bn

Industry - Packaged foods

LTM Revenue - €3.03Bn

LTM EBIT - €325.4m

LTM Net Income - €136.m7

LTM Free Cash Flow - €109m

As always, a new article means a new stock purchase. I’ve gone down the old value route with a relatively boring business named Nomad Foods. The appeal here comes from high insider ownership, a decade low valuation, high dividend yield & generous share buyback program showcasing their shareholder friendly return policy along with there dominance in the European frozen food market driven by their high quality and trusted brands. If your from the EU you’ll probably be familiar with their brands Birds eye, iglo and Findus.

Lets dive in.

A) Business and Industry

1) Geographical markets and brands

Headquartered in the United Kingdom. Nomad Foods is the largest frozen food company in Europe, operating a multi-brand portfolio across 22 European markets.

Their portfolio of brands include some of the most trusted and high quality frozen food brands being Birds Eye, Findus, iglo, Aunt Bessie's and Goodfella's. These brands are household names in their respective markets with a loyal following. In the 15 key markets in which they operate, they are ranked 1st in twelve for brand equity, brand awareness and customer preference.

Their operations span across Europe with their main markets being the UK, Germany, Italy, France, Sweden and Croatia, accounting for roughly 70% of the companies total revenue. Their main market, the UK accounts for just over 30% of the revenue through their brands Birds eye, Aunt Bessie’s and Goodfellas, followed by Germany accounting for 15% (iglo) and then Italy with 13% (Findus). Living in the UK I can confidently say their brands are highly popular and come with a reputation for high quality and superior taste. I can’t testify for Germany, Italy and other markets? Maybe some of my readers can give some feedback into these brands from their respective countries?

2) Shift change

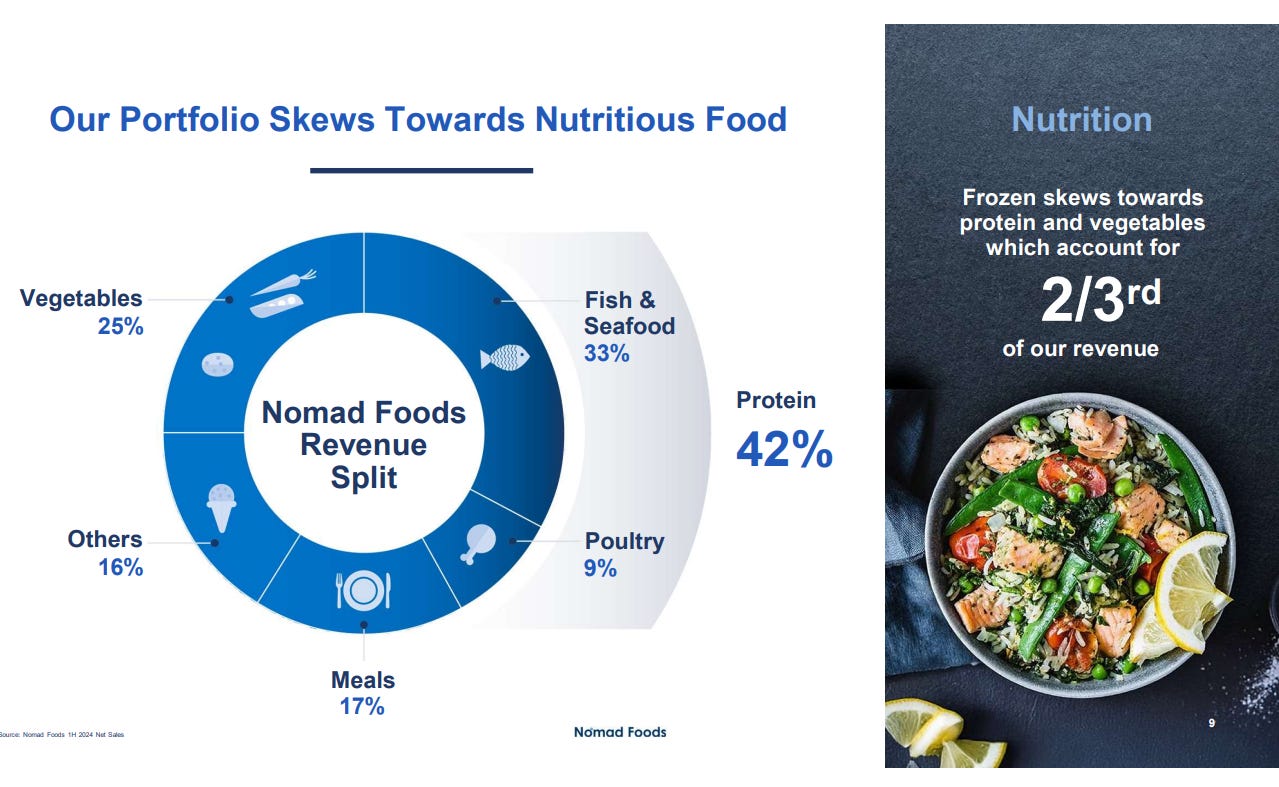

A common misconception amongst frozen food is the popular belief of them being unhealthy or their nutritional value aren’t as high as fresh alternatives. On the unhealthy topic, this might have been the case a decade ago but consumers today focus more on healthy alternatives with food manufacturers having altered and shifted towards this trend. Nomad is the perfect example. Nearly 70% of its sales come from protein and vegetables with further efforts into manufacturing healthier alternatives for their ready made meals. This trend should continue into the foreseeable future and Nomad is well positioned by increasing their expenses towards innovation to adhere to this increasing trend.

3)Market dominance and competitive threat

To highlight the companies market leadership and dominance in the branded frozen food category, they hold the #1 or #2 market share position in 90% of its core product categories across Europe. They also hold an 18% market share in the frozen food category which is nearly three times the size of its nearest branded competitor. Emphasis here on the “Branded”. The main competitive threat however is that of private label offerings which hold collectively a 35%-50% market share. This category has shifted from being a “budget conscious alternative” to becoming a dominant force in the European frozen food market with new premium offerings that can match the quality and taste of branded alternatives. This is a real threat to companies such as Nomad but there is a silver lining. The section of private label offerings which are considered “premium” don’t really compete much on price which keep branded companies in contention and on shoppers lists.

4) Industry

The frozen food industry is undergoing a significant transformation, evolving from a category once defined by "emergency" convenience to sustainable, and health-conscious lifestyles. The European TAM for frozen food with a 37% global share, is currently valued at roughly €75 billion. Industry experts forecast an annual growth rate between 4%-7% with an estimated TAM of €90 billion in 2030.

The image above highlights this growing trend. More consumers are shifting towards frozen alternatives and there’s a few reasons behind this.

Convenience - Consumers agree that frozen food provides some short-cuts compared to chilled/fresh food, thereby saving them time. With busier routines and longer work hours, modern life has made many consumers look for simpler ways to save time during meal prep. Frozen food is no longer seen as a low-quality alternative, but rather as a convenient and often healthier alternative to fresh produce.

Value - Frozen food is often cheaper, and with food inflation hitting high levels, consumers are switching to frozen to stretch their budgets.

Sustainability - Frozen foods generate significantly less waste than fresh alternatives, largely due to their extended shelf life and the ability to portion only what is needed. Also in supermarkets nearly six times more fresh foods are thrown away compared to frozen. Continuing on the sustainability front, frozen foods require less complex logistics and fewer trips reducing costs and emissions.

B) Competitive Advantages

I wouldn’t say Nomad Foods fits into the QUALITY category. By this I mean they face huge competition, moderate ROIC, have very limited pricing power for fear they might lose volumes and price inflation can affect the business short term as they catch up with pricing (A current headwind)

However, they’re a titan in the frozen food industry within Europe. Nearly three times the size of its nearest branded competitor— Nomad benefits from significant cost and logistics advantages along with strong relationships with the top retail partners making sure its products receive prime shelf space. They also hold brand recognition and their reputation is also high for quality and taste.

Taking away their most recent financials as they’ve recently been pressured by supply chain inflation, Nomads gross margin is among the industries best. They leverage their position as Europe’s leading frozen food company to drive margins through extreme operational scale, strategic procurement, and a high-efficiency manufacturing network. Its also boosted due to Nomads ability to gain maximum leverage with suppliers. In this game, a high gross margin typically indicates a sign of pricing power (To some extent ) and is also a sign of low cost advantages.

C) Fundamentals

In this section we look at the businesses fundamentals. Every investor has their preferences on which metrics to put focus on. Fundamental metrics change from company to company because businesses operate in different industries, face unique competitive landscapes, and are at different stages of growth. For Nomad we will look into their revenue, margins, cash flow generation, market leadership and balance sheet health.

1)Revenue

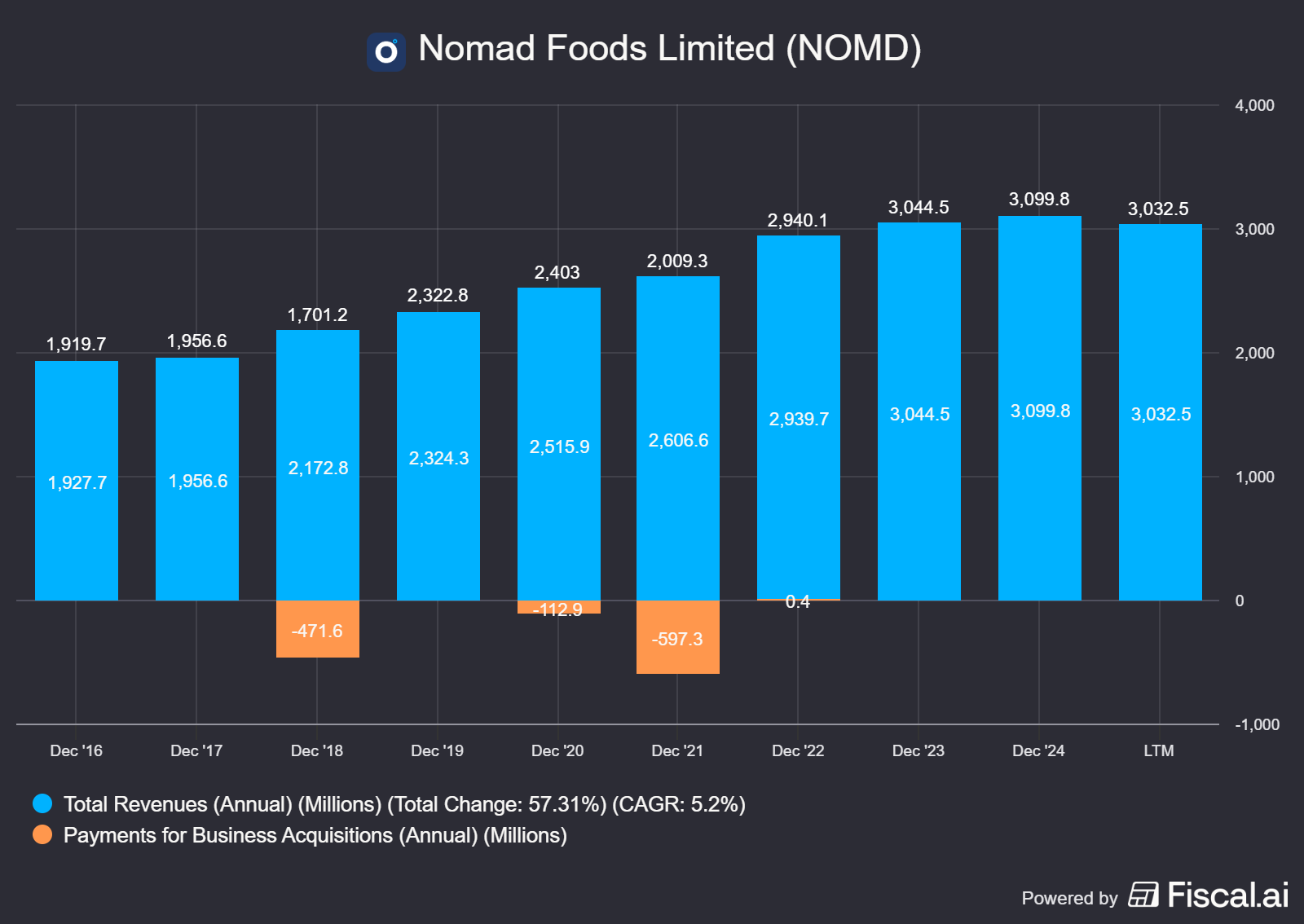

Nomad isn’t a high growth company, far from it. Contributors to revenue growth consist of increased market share, price increases and at times through acquisition. As you can see over the past decade around £1.2Bn has been deployed towards acquisitions which dramatically increased revenues the following year. The recent troubles facing the company is a combination of persistent volume declines, and intense competition in European markets especially from private label. Looking into 2026, the business is estimating a decline in revenues of between 2% and 5% mainly due to timing of their annual pricing negotiations with customers in which some are retaliating and also volume declines as the business increases it pricing to offset inflation from fish. Over the past decade revenues have grown at a CAGR of 5.2%.

2)Margins

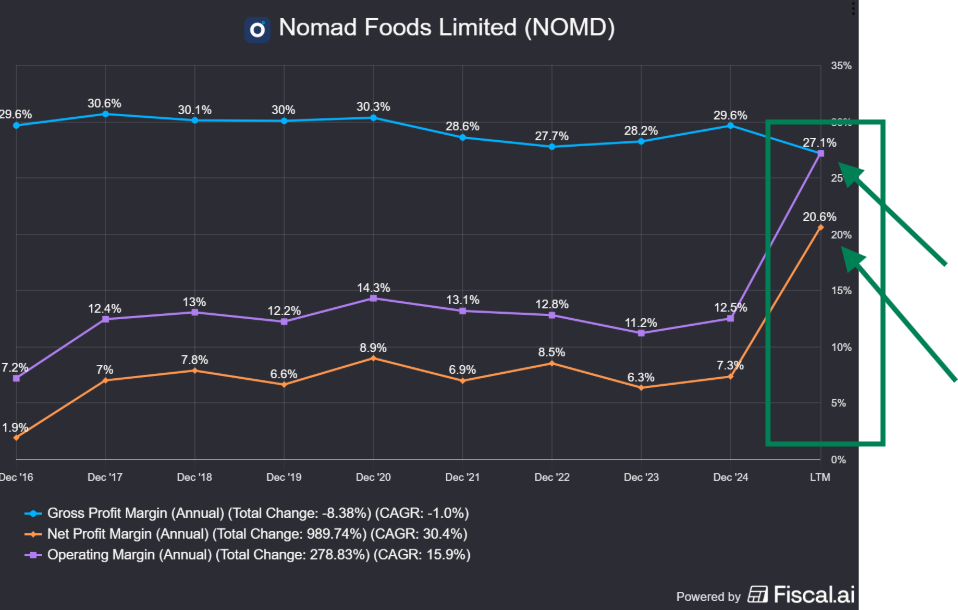

Nomads margins are industry leading. Over the past decade margins have been generally stable even through the rise of the private label competitive threat. This proves my point which mentioned earlier regarding private label premium products and pricing. Nomad might have lost share but pricing is relatively stable to due premium private label offerings being just as costly.

The reason for the highlighted area in the image above is due to some technical issue or just that the business isn’t largely covered by Fiscal AI and they haven’t updated their data. During 2025 Gross margins came in at 27.14%, a huge drop of 250+ bps from the prior year. This has been addressed in the most recent call with blame pointing at supply chain inflation with delayed increased pricing to customers not adequate to offset this. Negotiations are underway with price increases to customers for the upcoming year which will reflect in the gross margin in the mid term albeit there might be a slight delay to push through to the financials. This has also made its way through the financial statement down to the bottom line which came in at margin of 4.5%, way off their historical averages.

I have to emphasise the stock is currently trading at a decade low valuation and for good reason. But this opportunity wouldn’t be present without the issues I mentioned above. As an opportunist I believe the business is underearning and will eventually regain its earning power and investor confidence.

3)Cash flow

Cash Flow is by far the most important financial metric out there. Unlike GAAP accounting where non-cash items are deducted to produce earnings, Free cash flow is what the company actually produces in any given year. Nomad is a cash flow machine. To put this into perspective and why this investment appeals to me, Nomad is trading at a market cap of €1.23Bn Euros all while producing cumulative cash flow in the last 6 years of €1.02Bn Euros. This cash flow has been adjusted by taking out lease, interest and capital investments.

After a poor financial performance during 2025 with net income decreasing €90 million, free cash flow of €109 million was still produced resulting in a current FCF yield of 8.8%. Adjusting for this down year and using their median net profit margin of 7.15% the FCF yield could rise dramatically to 15.3% in the coming years at the current price. This is contributed by an adjusted increase of €80 million to the bottom line.

4)Market Leadership

The competitive landscape within the frozen food industry is intense. As I mentioned earlier Nomads main competitor comes in the form of private label offerings from big retailers collectively accounting between a 35%-50% market share. Private label, once considered for budget shoppers have shifted to offer premium offerings such as Tesco’s Finest, Morrisons Best of and Exceptional by Asda which have taken market share in recent years from branded companied such as Nomad. Since 2021 Nomad has lost 190 bps of market share to private label brands alone and was contributed due to price increases during the period of high inflation which led consumers to shift more budget friendly alternatives.

Nomad is currently in a transition period with plans through 2026-2028 to regain market share from private label brands. Through efficiency savings in which they plan to save €200m, Nomad plans to use on innovation of new products, increased marketing spend and data-driven promotional activity.

Nomad knows the importance and the change in consumer shift toward a more healthier lifestyle. Products such as Birds Eye Get Real Protein bowls, released in Sept 2025 is a recent example of how Nomad is targeting health-conscious shoppers with busy lifestyles with emphasis on protein and fibre content.

With their trusted brand reputation for quality and taste, I believe Nomad foods is capable of regaining market share from their branded and private competition. The key is to showcase their value proposition through their high quality foods by making consumers trade up rather than down to lower alternatives.

5)Balance sheet

Turning to the companies financial health, Nomad has a relatively stable but leveraged balance sheet. Its debt currently sits at €2.25bn and while this debt load is considered high, Nomad consistently produces strong cash flow generation to service these debt levels. This might not be the company for risk averse investors who prefers minimal debt.

Cash and Cash Equivalents - Readily available cash. Nomad currently has €324 million. Well within capacity for the company to pay liabilities in the short term and to fund the business operations.

Long term debt - Outstanding debt. Nomad debt level has slightly increased since the Q4 2024. Debt currently sits at €2.25 billion. During 2025 the company refinanced the majority of this debt all the way through to 2032, a strategic move as they are currently undergoing some financial pressure. Doing this they only have one outstanding tranche of €800 million due June 2028.

Current ratio - Measures a company’s ability to pay off its short-term liabilities (debts and obligations due within one year) with its short-term assets (cash and assets expected to be converted into cash within one year). Nomads current ratio is adequate sitting at 1.07. Total Current Assets: €1,146.8 / Total Current Liabilities: €1,067.9 = 1.07 ✅

Debt / Equity - Debt/Equity ratio is a primary measure of solvency risk. A higher number here typically >2x is considered highly leveraged and more at risk of insolvency. Their current D/E sits at 0.92 which is considered healthy within their industry.

Interest ratio - Shows if a company’s earnings (EBIT) is sufficient to pay the interest on its debts. 2025 EBIT totalled €325 million and interest expense came in at €116 million which gives an interest ratio of 2.81x. This is considered safe but less than my preferred target of 4x. This lower interest ratio was less during 2025 due to lower profits during the year. I expect this ratio to rise within my target range in the coming years when the company starts to realise price increases and cost savings boosting profitability

Conclusion

Although Nomad has large debt levels they are consistently generating large amounts of cash to service it. Also, the majority of debt maturities have been refinanced all the way through to 2032, a good strategic move from management. Only one tranche of €800 million is due in 2028.

D) Capital Allocation

Nomads capital allocation priorities are as follows. Invest in the business, acquisitions, buybacks and dividends — Only up until recently.

Nomad first priority is to invest in the business. 2026 will be a transition year for the business as they are funding an efficiency program aimed at saving €200 million which will be put back into the business for growth by increasing its investments in innovation and marketing in an attempt to win back share from private label.

Currently shareholder returns are a key focus specifically through dividends and aggressive share buybacks due to what management perceives as a significant undervaluation of the company's stock.

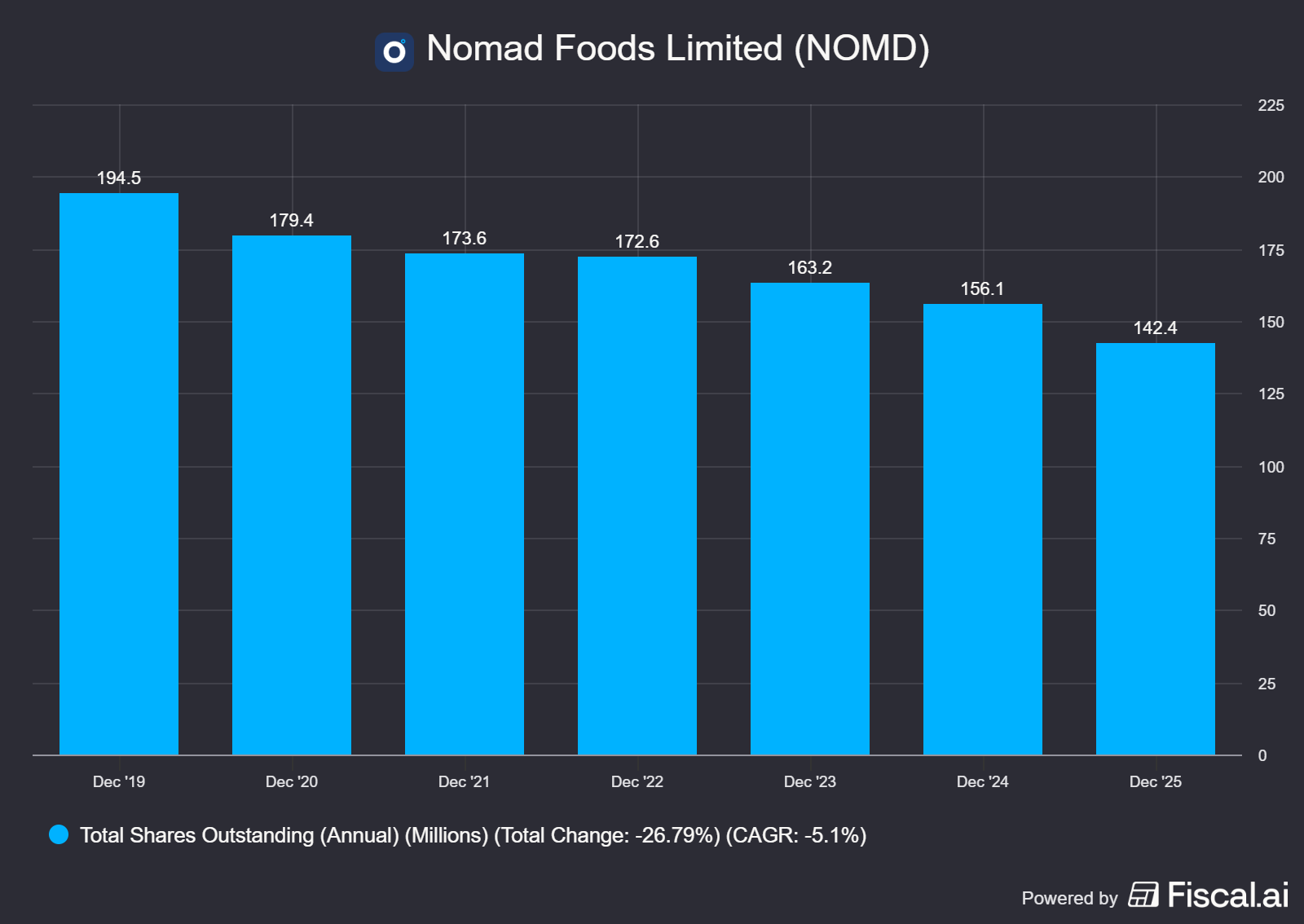

During 2025 Nomad returned €287 million to shareholders through a combination of dividends and repurchases, retiring approximately 9% of outstanding shares by year-end or a total of 14.1 million shares. On the belief of managements thoughts on the stocks undervaluation. They had this to say in the most recent earnings call.

From CEO Dominic Brisby

“Just to put this in context, a measure of how much I believe in this business and how much Ruben (CFO) believes in this business is the fact that over the coming weeks, we're both going to be making substantial share purchases in the company.”

“As you know, buybacks have been a priority for us, as we believe that our shares are trading well below their intrinsic value, and we continue to have an appetite to repurchase shares at current prices”

“I see a clear path to create tremendous value for our shareholders and intend to make a sizable open-market purchase of Nomad shares in the coming weeks to express my confidence and align my interests with our shareholders.”

These are just some of what the CEO has put out there to the public.

$151 million remains under the current repurchase program of $500 million. I expect this to be completed by its 2026 end date. At current prices and if they use the full $151 million allocation then roughly another 10.7% of shares could be retired. Below shows their aggressive stance on buybacks repurchasing 26.7% of outstanding shares since 2019.

On to Dividends — Nomad initiated its first-ever quarterly cash dividend on January 30, 2024 and currently pays out $0.17c quarterly or 0.68c on an annual basis. This dividend is well covered by cash flow and currently yields an impressive 6.8%. Even with 2026 being labelled as a transition year, management has stated its commitment to its dividend policy.

Nomads acquisition strategy seems to come in chunks. Over the past decade, a total of €1.18Bn has been deployed into the following business acquisitions.

Goodfellas pizza - £200m

Aunt Bessie’s - £210m

Findus Switzerland - €110m

Fortenova frozen food - €615m

Nomad isn’t as active on the acquisition front mainly due to their disciplined acquisition approach, leading a patient-led strategy rather than rapid expansion. Management evaluates targets based on several non-negotiable factors.

Targets must be market leaders either #1 or #2 in share within their niche segments.

Strong cash generation.

A reasonable Valuation.

It is believed there’s a compelling pipeline of acquisition targets but management maintains discipline by walking away from numerous deals that do not meet their specific quality or valuation tests.

Conclusion

Nomads capital allocation priorities always prioritises growing the business. However, due to the recent headwinds followed by a dramatic drop in share price, management have shifted its focus on returning capital to shareholders through share buybacks. This is evident by the large amount of capital deployed towards buybacks in 2024 and 2025. To put this into perspective 21.3 million shares have been repurchased or 13.8% of shares outstanding during these two years for a total cost of $348 million. $151 million remains on the current program that ends late 2026 which could retire another 10.7% of shares at current prices. I cant see any acquisitions being completed during 2026 as the company navigates through their transition year and back to normalised profitability and growth.

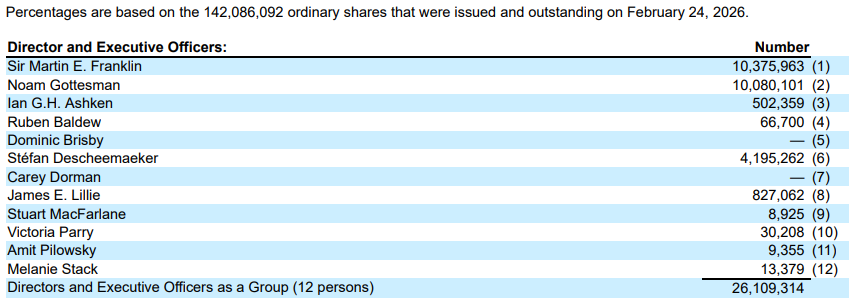

E) Insider Ownership

Insider ownership is a major green flag whenever analysing a business. This tells the investor that executives of the business have “Skin in the game” that their interest aligns with that of shareholders. This skin in the game — will incentivise management to focus on long-term projects rather than short term targets that usually destroy true shareholder value.

Nomads insider ownership is impressive. Insiders own a total of 18.3% of the outstanding shares as of 24th Feb 2026. The largest of these are the co-founders Noam Gottesman and Sir Martin Franklin who collectively own 20.4 million shares. Gottesman and Franklin are still both heavily involved at Nomad and are both co-chairman of the board. Another large owner is S.Descheemaeker the former CEO of Nomad who retired in Jan 2026.

Dominic Brisby who is current CEO hold zero shares here as he’s only been in the role a few months. He has stated however how he and Ruben are planning to make “Substantial” purchases in the open market in the coming weeks.

F) Valuation

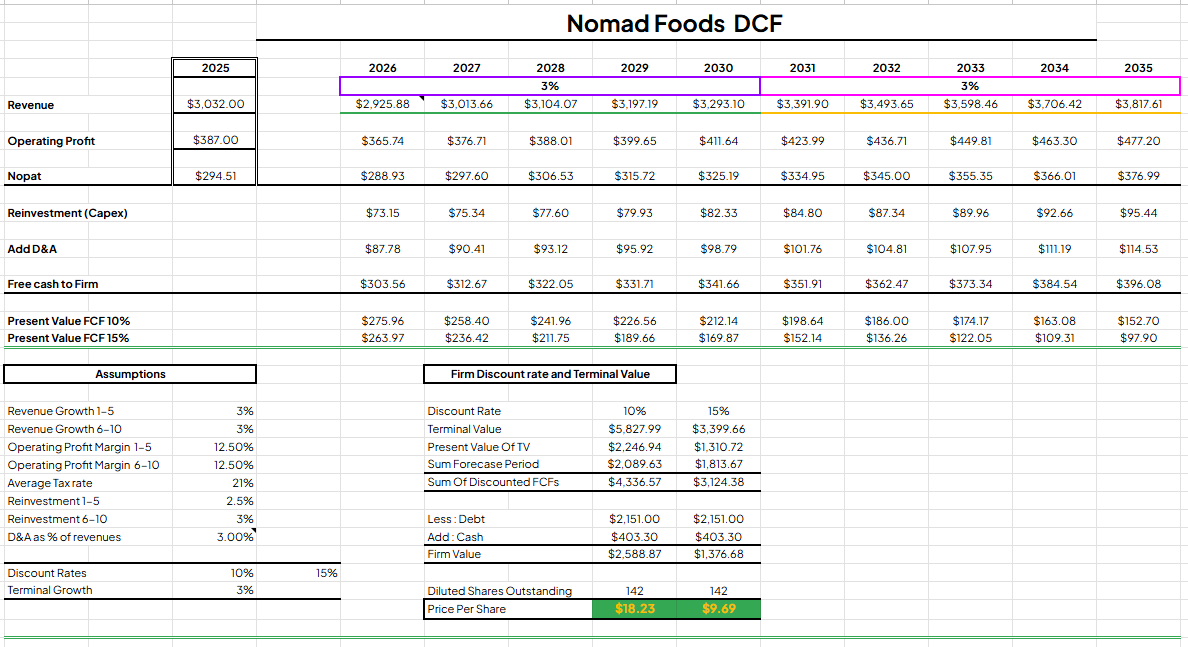

Below is my discounted cash flow valuation for Nomad foods using both 10% and 15% discount rates.

Assumptions

Revenue growth - 3%

EBIT margin - 12.5%

Tax rate - 21%

Terminal Growth - 3%

With these fairly conservative assumptions Nomads fair value is $18.23 on a 10% discount rate and $9.69 (Around todays price) for a 15% discount rate. These tell us that if the assumptions are correct then the business is seriously undervalued on a 10% IRR basis and fairly valued on a 15% IRR.

Risks — Obviously these assumptions come with risks. Capital structure could change increasing its net debt position which will reduce the firms value, revenue growth might not materialise as they could continue to lose volumes to private label competitors, their efficiency program could fail and margins might not recover to previous heights. I do believe however, investors are slightly protected by Nomads high insider ownership and their priority and consistency of returning cash to shareholders through aggressive buybacks and their high yield dividend.

G) Conclusion

First off ……… even a great company is a bad investment if you pay too much. Nomad foods isn’t your usual sexy stock that gets well-publicised throughout media channels. They operate in a boring industry, their growth is relatively low and they produce low margins but ……… a successful investment doesn’t have to have all the highest metrics and expectations. To the contrary. For an investment to become a successful one I believe it must have the following criteria and there’s only three.

A large miss-pricing from its intrinsic value to its current price.

A leader operating in a resilient industry that’s protected from obsolesce.

ROIC ex Goodwill > WACC.

I can confidently say that I believe Nomad passes all these criteria. We’ve seen the valuation and the resilience of the industry needs no introduction. You might ask, why I’m using ROIC ex Goodwill. The reason being is that Goodwill is capital allocation decisions of previous management and takes into account intangible assets into the denominator. I prefer excluding goodwill as we get so see the true economic efficiency of the business with its current tangible assets. Nomads LTM ROIC ex goodwill came in at 14.4% which tells us for every $1 of tangible assets they produce 0.144c in cash.

Other confidence factors come in the form of their high insider ownership from the co-founders and the executive team and their highly aggressive shareholder return policy.

This investment wont be for everyone, hardly any if I’m completely honest as many investors today prefer high growth, high margin, recurring revenues, high ROIC and operating in a long term growth industry but these come at lofty prices. Nomad could work for the investor who truly looks for undervaluation and looking for yield in the form of buybacks and dividends.

Thank you for taking the time read the article.

Hopefully you’ve learnt something new.

DInvests

I hold a beneficial position in Nomad Foods NOMD 0.00%↑ . My buys and sells aren’t recommendations. I can’t guarantee the accuracy of the information provided in the newsletter. All statements express personal opinions and information gathered online. Any estimates, forward looking statements and assumptions made in this newsletter are unreliable. Always do your own research. Any information in this newsletter is for educational and entertainment use only and should not be taken as investment advice.

I live in Germany and can confirm iglo is quite popular and present in the major chains here. I am very bullish on the sector since frozen foods are usually fresher than the "fresh" food offered in the supermarket and health consious people are starting to get aware of that. You can also check out Frosta, a German competitor. More profitable but also not nearly as cheap as Nomad. Thanks for the writeup!

Hey D. NOmad foods hoklder here. I have subbed. Let’s support each other and grow together. Check my latest article on UBER here https://substack.com/@valueinvestorfromitaly/note/c-232679105?utm_source=notes-share-action&r=3qdo3i