New Buy : Zoetis 🐕

From Premium Growth to Value Play: The Investment Case for Zoetis in 2026

Summary

Name -Zoetis

Ticker - ZTS

Market cap - $33.3Bn

Industry - Pharmaceuticals

LTM Revenue - €9.46Bn

LTM EBIT - €3.6m

LTM Net Income - €2.6Bn

Investment opportunity

After a significant drop in share price, I believe Zoetis presents as an attractive investment opportunity. The business ticks many boxes within my investment strategy.

A leader in a niche market “Animal health” ✅

Resilient business model ✅

High barriers to entry ✅

Attractive margins and excellent ROIC with future growth runway to deploy more capital at these high returns ✅

As the global leader in the animal health industry, Zoetis benefits from the “humanization of pets” trend, which drives resilient demand for premium companion animal products, while its strong presence in the livestock sector provides further geographic and species diversification. With high operating margins, a robust R&D pipeline targeting significant unmet needs like oncology and chronic pain, and a consistent track record of returning capital to shareholders through dividends and buybacks, I believe Zoetis is well-positioned to remain a durable compounder going forward.

Before we dive into the business, first we need to address why the stock has declined so significantly.

In a nutshell, Zoetis story “might” have changed. The old investment thesis “and when Zoetis was trading at huge premium” centred around a business that was unique with innovative drugs that nobody else could compete, pet owners would spend on their pet regardless of the state of the economy and constant price hikes that customers would pay for premium products. The new story looks a little different …….

Zoetis might never get back to its previous multiple when the moat looked solid. There’s no doubt the resilience of its business wasn’t as strong as once thought and competition is heating up. Its fair to predict that going forward a lower multiple is acceptable. However, I believe the decline in share price has been a bit too excessive. As of writing, its trading at approx. 10x EV/EBIT. Zoetis is still the industry leader with premium products supported by reputation and quality which Veterinarians, livestock producers, and pet owners rely on for safe, effective, and reliable solutions which translates into high retention rates. A high quality pipeline researching unmet therapies with a focus on being “first to market” and their savvy strategic acquisitions into digital solutions which is making their business model stickier as Vets are adopting these solutions into their daily workflows which should protect the businesses competitive moat going forward.

A) Business

Zoetis is the world’s largest company dedicated to animal health. Spun off from Pfizer in 2013, it has grown into a powerhouse, generating $9.5 billion in revenue with a massive portfolio that includes over 15 "blockbuster" products (meaning each generates more than $100 million in annual sales) They provide the medicines, vaccines, and diagnostic tools that veterinarians and livestock farmers need to keep animals healthy and well-cared for. From everyday check-ups for family pets to large-scale health management for livestock, Zoetis creates science-based solutions that help prevent, detect, and treat diseases, ensuring a healthier future for both animals and the people who care for them.

🔶 Segments

The company divides its business into two primary segments based on the type of animal:

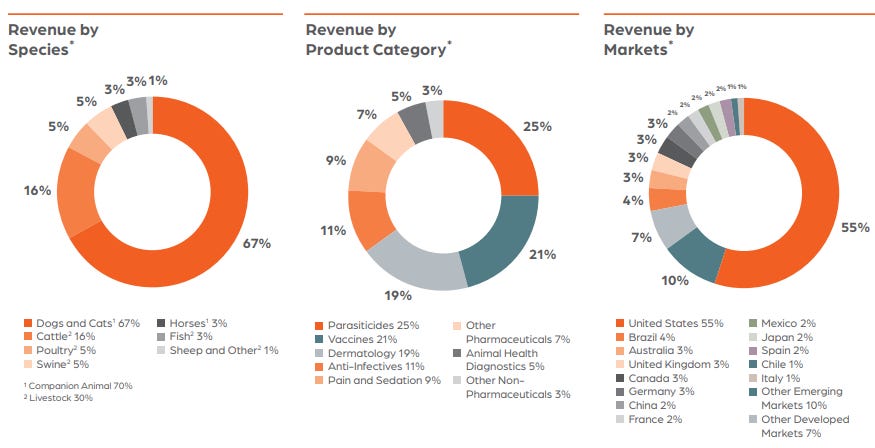

Companion Animal: This is the primary driver of revenue, accounting for approximately 70% of total sales. This segment includes products for dogs, cats, and horses.

Livestock: This segment contributes approximately 30% of total revenue and includes products for cattle, poultry, fish, swine, and sheep.

🔶 Key Product Categories

Zoetis categorizes its portfolio into six major areas, which collectively cover the “Continuum of Care” (prediction, prevention, detection, and treatment). The top three which contribute to 65% of total revenues are;

Parasiticides: Preventive treatments against parasites such as fleas, ticks, lice and worms. This is their largest category accounting for 25% of total revenues and is the industry leader in the space with their Simparica franchise, a monthly chewable and their largest blockbuster. Zoetis continually innovates to produce product line extensions, most recently introducing Simparica Trio. This drug extension includes fleas and ticks (the target for their legacy Simparica) with the addition of heartworm and intestinal worms. The goal for Zoetis is to focus on "label expansions" for its existing, trusted products.

A quick intro on label expansions for those who aren’t familiar with the term. In simple terms, a label expansion is like giving an existing medicine a "promotion" or "new job description." It means the company has done enough additional testing to prove the drug is also safe and effective for something new. Below is an example of Simparica. Initially the drug was meant only for Fleas and Ticks. The expanded line Simparica Trio includes worms which results in broader protection and convenience for the pet owner. Label expansions are researched to bolster a product's position in the market and can “at times” be a case for a secondary patent filling and make it more difficult for competitors to make generics as they have to navigate through multiple layers of intellectual properties.

Vaccines: These are Biological products for disease prevention accounting for 21% of revenues. Here, Zoteis offers pet owners and livestock producers essential vaccines for protection of animals from common and life-threatening diseases. They also offer "Risk-Based" (extra protection for specific environments) which might get recommended by vetinarians for animals based on their specific lifestyle or breed.

Dermatology: Solutions for skin conditions (e.g., Apoquel, Cytopoint) which make up 19% of revenues. Zoetis provide industry-leading treatments which are targeted for canines, such as Apoquel (a daily tablet) and Cytopoint (a long-lasting injection), which are specifically designed to stop the "itch cycle" and provide immediate relief for dogs suffering from allergic skin conditions.

Other categories include;

Anti-Infectives - products that prevent, kill or slow the growth of bacteria and fungi.

Pain & Sedation - products that alleviate pain, primarily associated with osteoarthritis and postoperative pain.

Animal Health Diagnostics - A comprehensive suite of tools and technology designed to help veterinarians detect, diagnose, and monitor animal health conditions with greater speed and accuracy.

Collectively these “Other categories” account for 35% of total revenues. Zoetis is highly diversified and not overly reliant on a single category. Most therapies are recurring in nature which makes Zoetis a highly resilient business during economic downturns as pets, regardless of the economy and if prescribed with Zoetis products will continue to use them rather than switch to a less reputable generic.

🔶Diversified business

Zoetis has a global footprint that spans more than 100 countries offering animal solutions in eight core species, including companion animals (dogs, cats, and horses) and livestock (cattle, sheep, swine, poultry and fish). This broad array of species and geographies, ensures that the company is never overly reliant on a single market or product cycle. While the United States remains its largest individual market, the company maintains a massive, highly capable International segment that captures growth in both developed and emerging economies like Brazil. This broad geographic spread acts as a buffer. If economic headwinds or competitive pressures affect sales in one region, the company can often offset that weakness with strength in others. This quarter acts as the perfect example. International revenues grew 17% y/y (10% organic) with livestock growing 7% globally while the U.S segment declined 8% and companion animals in the US declined 11%.

Other advantages include the essential non-discretionary spending on companion animals and when emergencies arise and livestock producers “must” spend to prevent illness among their herd. Both these drivers create a powerful foundation for revenue stability during economic downturns.

Even though Zoetis is highly diversified, they are not immune to growth headwinds. By looking at the image below, we can see where Zoetis is exposed. The US represents 55% in annual revenues with dogs and cats representing 67% by species. Lower disposable income among pet owners can dampen growth. This was the case in Q1 2026. Revenue in the US declined 8% whilst U.S. Companion Animal segment revenue dropped by 11%. Reason ……… pet owners have become more cost-conscious, leading to a decline in veterinary clinic visits, reducing discretionary spending on pet healthcare or pet owners are opting for lower priced generics. The market hates uncertainty which is the reason for the huge decline in stock price. This weakening of moat has really hurt the stock.

B) Competition and Competitive Advantage

🔶Competition

Zoetis operates in a highly competitive global animal health market, where success is driven by intense research and development, continuous innovation in biologics and precision medicine, and the ability to maintain strong, direct relationships with veterinarians. Rivals frequently challenge Zoetis by launching competing products in key high-growth segments like dermatology and parasiticides “A current headwind”

Key Competitors

Merck Animal Health (MSD Animal Health): Third largest in revenues and a division of Merck. They compete with Zoetis across nearly every major category and geography.

Elanco Animal Health: A significant competitor that frequently targets Zoetis’s market share in dermatology and parasiticides with aggressive new product launches and combined-action formulas.

IDEXX Laboratories: The primary competitor within the diagnostic space. IDEXX is the most direct threat to Zoetis’s diagnostic ambitions. They set the industry standard for reference laboratories and in-clinic analysers.

Boehringer Ingelheim: Second largest in revenue and a major rival, particularly strong in livestock vaccines, biologics, and parasiticides.

Out of the major rivals listed above. Merck and Boehringer have near the same scale and R&D capabilities as Zoetis. Elanco competes in more niche therapeutic areas and IDEXX through their digital solutions. Competition is heating up and Zoetis has seen market share being taken as price conscious pet owners are opting for cheaper generic brands over Zoetis premium products.

🔶Continuum of care

Zoetis’s "Continuum of Care" is a strategic framework designed to lock in veterinarian customers into an integrated ecosystem by providing solutions at every stage of an animal's health lifecycle: predicting, preventing, detecting, and treating disease.

Predict

Prevent

Detect

Treat

Rather than selling isolated products, Zoetis bundles its offerings—such as genetic testing, vaccines, diagnostic hardware, and specialty therapeutics—to create a "sticky" relationship with veterinarians and livestock producers. This approach makes it difficult for competitors to replace Zoetis because they would have to displace the entire integrated workflow rather than just a single pill or vaccine.

Zoteis move into the diagnostic area in 2018 bolstered Zoetis business model and integrated their offerings to a full-spectrum solution which is designed specifically to build the “sticky” ecosystem as mentioned above that also captures recurring revenue. All four pillars work together to diagnose and treat companion animals through advanced data and AI. The data gathered at the “Predict“ and “Detect“ stages informs the application of products in the “Prevent“ and “Treat“ stages. This integration makes the company’s solutions more effective and builds stronger relationships with veterinarians. The installed products creates a razor blade business model as all their instruments are “proprietary”, “closed” systems. Meaning, once consumables are used vets must purchase consumables directly from Zoetis to ensure quality and calibration. You cannot use reagents, test rotors, or testing cartridges made by other manufacturers in Zoetis machines. Although this revenue pool is small relative to other categories, its ambition is to create even stronger relationships with their customers that will protect and make other categories more resilient in the future. The growth runway ahead is large.

We could ask why would a veterinarian adopt Zoetis’s diagnostic equipment?

There are some huge benefits. Once a veterinarian adopts Zoetis diagnostics tools, instantaneously their practice becomes more efficient and precise. Ultimately this improves clinical outcomes, operational efficiency, and staff well-being as workloads are reduced allowing veterinary teams to spend less time on administration and logistics. They’re also able to diagnose a condition on the day of a patients visit rather than wait days for lab tests to return through a third party. Other benefits include Zoetis “Virtual Laboratory.” If a vet encounters a difficult case, they can digitally share images or data with board-certified clinical pathologists or specialists, often receiving expert feedback within hours rather than days. The advantages are huge. Vets want to diagnose pets accurately. After all, reputation is everything in this industry and partnering with Zoetis, the industry leader only strengthens this.

🔶 Research and Development

R&D is a critical component and is a primary engine of future growth. Zoetis, being the largest animal health company must stay ahead of innovation or risk losing share to competitors. By continuously innovating, Zoetis maintains its market leadership which supports its premium pricing strategy while also addressing the unmet medical needs of pets and livestock.

As with any company in the medication industry, its important to continuously invest in existing products through label expansion to defend against generics and new products that have yet to be marketed and are less researched. Zoetis focuses on "first-to-market" innovations in low penetrated therapeutic areas like chronic kidney disease, oncology, cardiology, and osteoarthritis pain in animals. If and when these pipeline drugs come to market, being the first, Zoetis instantly takes large market share and obtains premium pricing.

Looking into the pipeline, Zoetis has more than 12 potential blockbuster candidates in development to offset competitive pressures and expand into new unmet therapeutic categories. However, none are due to be released this year. The anticipated approval for long-acting Cytopoint is towards the end of 2026 with launch early 2027. “Cytopoint, a dermatology treatment that’s administered by the vet which gives dogs relief 4-8 weeks” The new long acting Cytopoint is anticipated to exceed the stated 4-8 week current period for the original Cytopoint which “should” trump Elanco’s newest dermatology product which lasts 6-8 weeks. In 2027, another potential approval for Zoetis is a debut drug in chronic kidney disease representing a significant advancement over current supportive-care-only options. If approval is granted Zoetis will benefit once again being the “First mover in this space”.

CFO Joseph Wetteny

“As we look ahead, we have a number of launches and approvals in terms of life cycle innovation that's going to contribute to our growth. And then we're anticipating the new big areas to start to get approvals towards the back half of next year to start the new innovation cycle, if you will for the company.”

🔶Patents

Patents give Zoetis exclusive rights to proprietary molecules, vaccines, and diagnostic technologies for a defined period. They ensure the company can recoup its R&D expenditures and earn a good return on capital for risks taken before competitors can produce lower-cost generics. This ultimately crates high barriers to entry allowing Zoetis to maintain high profit margins.

Looking into the companies 10-K, Zoetis does not publicly provide a consolidated "list" of all patent expiration dates for its entire portfolio.

Unlike human pharmaceuticals “Patent cliffs” aren’t as dramatic in the animal health industry. This is due to innovation cycles, technological barriers and customer relationships. First … Cytopoint, Librela, and Solensia—are monoclonal antibodies. They are notoriously difficult to replicate. Even if a patent expires, a competitor cannot simply "copy" the chemical formula. They must master the proprietary, highly sensitive, and expensive manufacturing process required to grow these proteins at scale. This "manufacturing moat" keeps competitors at bay for years.

For investors, the risk is usually not an expired patent, but rather a superior new product. As with any pharma company, the primary defense against patent-related revenue loss is to aim to refresh their portfolio faster than their legacy products can be challenged. With 12 blockbusters in the pipeline in new, unmet therapies along with label expansions the firm seems in good shape for the future to continue its market leadership. Animal health is a relationship-driven business. Veterinarians often stick with a branded, trusted product they know is safe and effective, even if a slightly cheaper alternative appears.

C) Financial Fundamentals

In this section we look at the businesses fundamentals. Every investor has their preferences on which metrics to put focus on. Fundamental metrics change from company to company because businesses operate in different industries, face unique competitive landscapes, and are at different stages of growth.

🔶Revenue

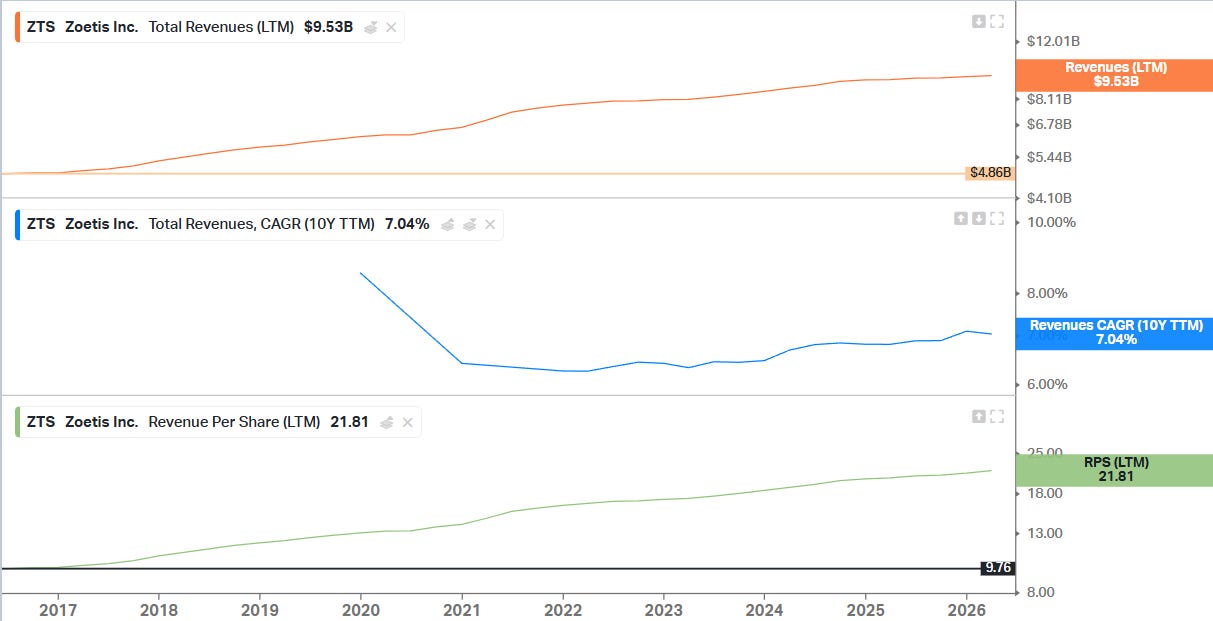

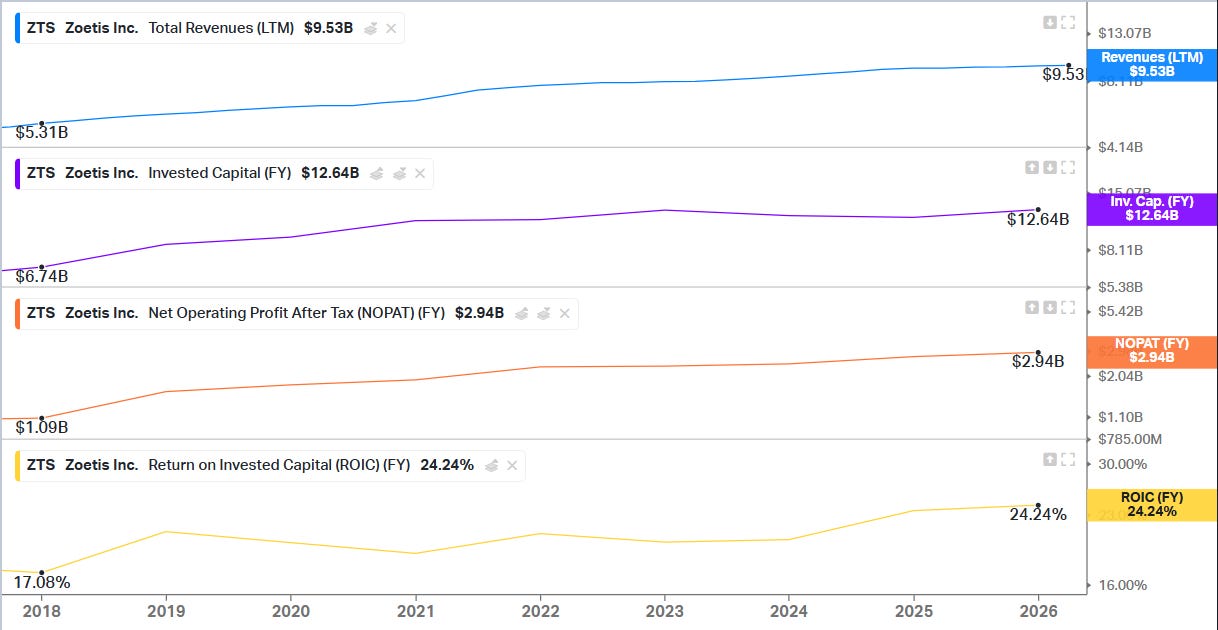

Revenues have grown from $4.86 billion in 2016 to $9.53 billion over the LTM. Annual CAGR has been fairly consistent at 7.04% over the last decade and within their long term target. Zoetis, through their shareholder return policy regularly repurchase shares. As the image below highlights, revenue per share has grown from $9.76 to $21.81 resulting in an annual CAGR of 8.37%. Over time, revenue growth will be tied to market share gains, new product launches and price increases. I don’t believe Zoetis will be a double digit revenue grower in the future. They are more likely to grow in the mid to high single digits as they have done in the past. As no new product launches are due in 2026, added with intense competition and price conscious pet owners, revenue growth will me materially lower this year. On a brighter note, we still have to acknowledge the strong brand loyalty, high barriers to entry, customer stickiness and a business model that prioritizes innovation which will continue to bode well for the business, producing revenue growth that will compound going forward.

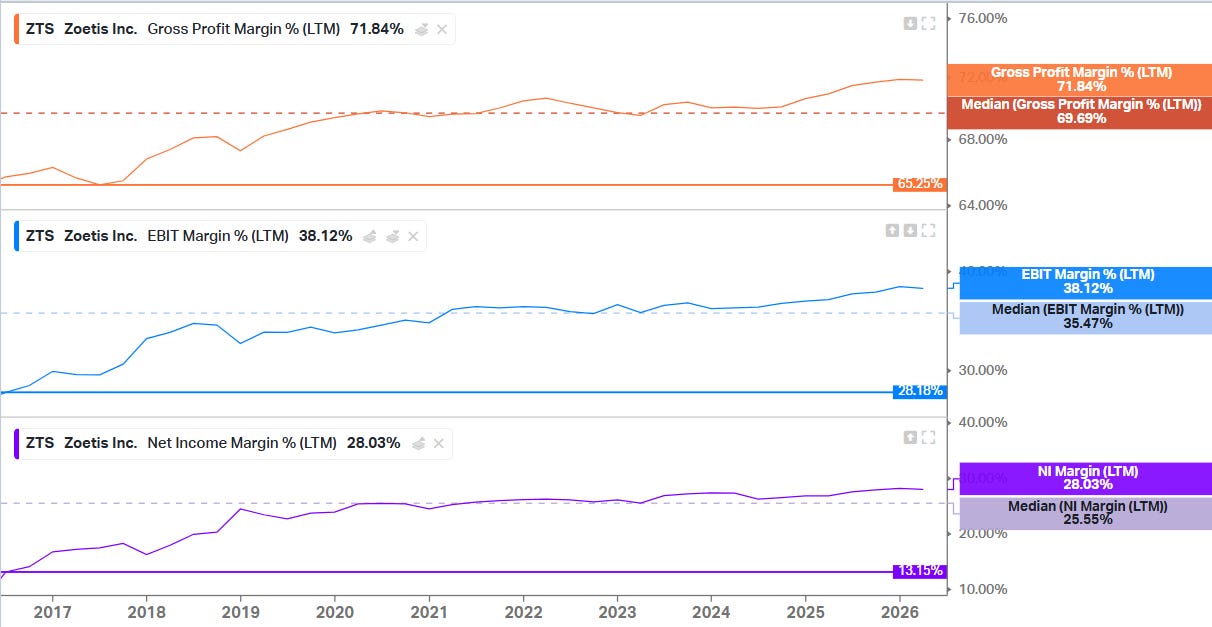

🔶Margins

Below are the 10 year charts for Zoetis Gross, EBIT and Net Margins. The charts clearly show a significant increase in all three. Below I’ll highlight the main reasons as to why.

The “Companion Animal” Shift - The most significant driver of margin expansion has been a product mix shift towards more companion animal product sales. Companion animal products command significantly higher price points and profit margins compared to traditional livestock products and which contributes to 70% of 2025 sales. Although the "humanization of pets" and increasing pet ownership provided the tailwinds that make the market attractive, Zoetis has intentionally used its capital, R&D, and acquisitions toward this segment to capture higher margins and more durable, recurring revenue.

Structural "Lock-In" through Diagnostics - Entering into the diagnostic space in 2018 created an integrated "ecosystem" where the diagnostic result leads directly to a Zoetis prescription, effectively controlling the customer journey from detection to treatment.

Direct to consumer marketing - Intentional direct marketing to pet owners has created brand equity. This has benefitted the business as pet owners walk into a vet clinic and specifically ask for a Zoetis product such as Simparica Trio instead of relying on a veterinarians to recommend the product.

Higher margins through biologics - Biologic products such as Librela, Solensia and Cytopoint command higher margins than small molecule drugs. These speciality therapies are usually “first of its kind” which ultimately allows Zoetis to demand premium pricing. These products are highly innovative and complex to manufacture which creates another level of protection once a patent expires, especially to competitors who do not have the capital power that Zoetis has.

🔶 Cash flow

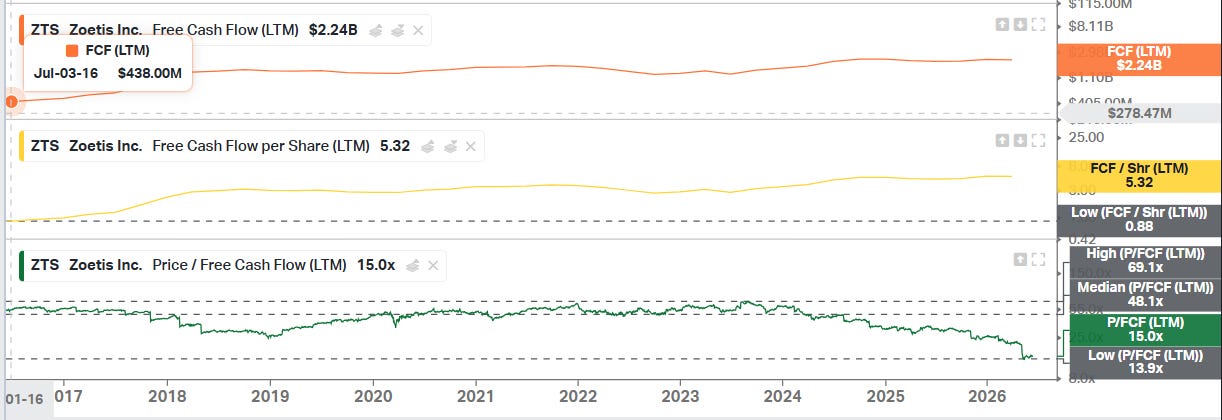

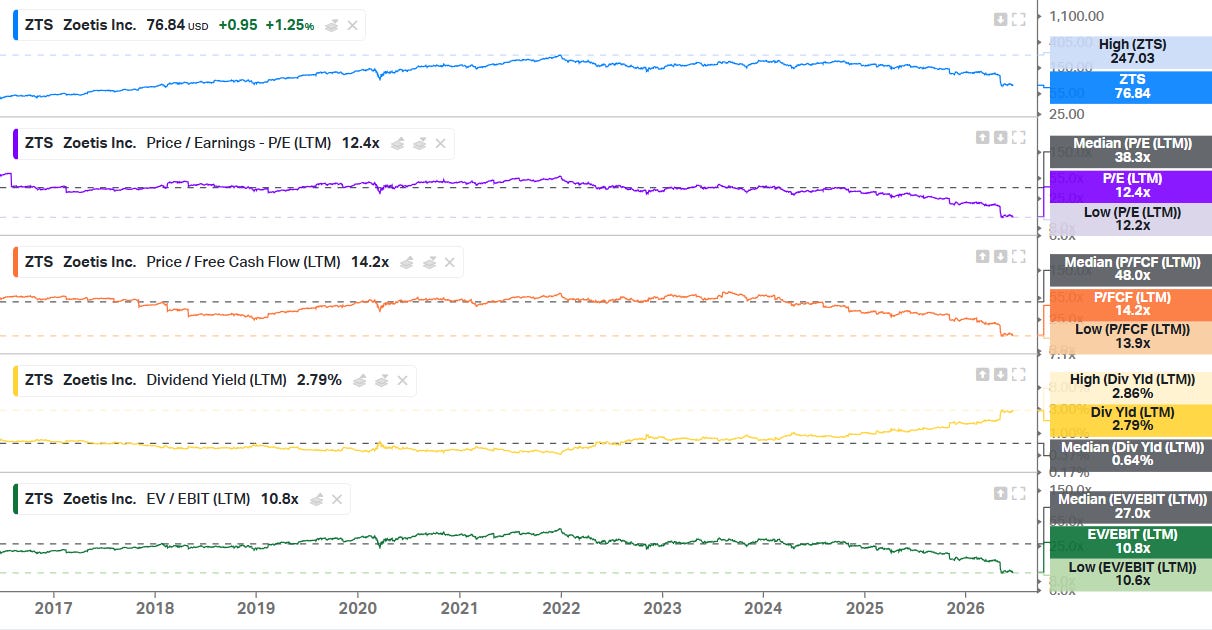

Zoetis is a cash cow. As with any investment, its so important how much we pay for a business. Zoetis has always been highly rated by the market and was once considered as an untouchable “compounder”. We can see how highly it was rated. The median P/FCF currently sits at 48x, this basically means if you’d have dollar cost average Zoetis stock over the past decade then you’d have approx. costs basis on a FCF basis around this number. Currently the business is trading at a 15x FCF multiple and recently hit its lowest valuation in over a decade.

I’m an opportunist. Very rarely do I purchase businesses that are trading at all time high multiples and are placed in a category of “pay whatever price”. Give me a business in crisis but with a solvable problem any day. Zoetis fits into this category and is why its in the portfolio today.

Looking into the growth rate of FCF/share Zoetis has grown from $0.88 to $5.32 or a 10 year CAGR of approx. 19%. This has been the result of a few highly beneficial catalysts.

Innovation of new products

Intentional portfolio mix shift towards companion animal

Share repurchases

Cost disciple and manufacturing scale

All these have contributed to the exceptional growth in FCF over the past decade. As we look into the future and something maybe the market is cautious on is the future growth rate of this FCF?

I’m a realist and in no way do I expect the company to continue on this growth trajectory. However, I do expect net income to grow in line with revenue growth which should be mid single digits, added to this the annual share repurchases and we should get a high single digit increase in FCF/Share in the future.

To put this into perspective, currently Zoetis is trading at a market cap of £33.3Bn while producing FCF of $2.24Bn, a very reasonable price to pay for this wide moat business. Below is the business percentile ranking over the last 10 years.

🔶Return on Invested Capital (ROIC)

Return on invested capital is considered a key metric and measures a companies ability to create value from the capital it deploys. Zoetis boasts superior ROIC. With a mean over the last 10 years hovering over 20%. These high returns are supported by the companies patented biologics and trusted global brands alongside a resilient, high-margin revenue stream from both companion animal and livestock markets.

On its own, ROIC means nothing. We have to measure the economic spread between its cost of capital and its ROIC. Zoetis again, has a large spread between the two showcasing they create significant value, a common trait among many high quality compounders.

Economic Value = ROIC - WACC “Estimate”

Economic Value FY 2025 = 24.24% - 7.05%

Estimate Economic Value = 17.19%

To keep up this trajectory of consistently high ROIC, Zoetis will have to keep innovating, being first to market, safeguard its reputation and continue its deep relationships with its customers. This way, the company will be able to grow its revenues and demand premium pricing for its products. Something they’ve managed and mastered in the past.

🔶Balance sheet

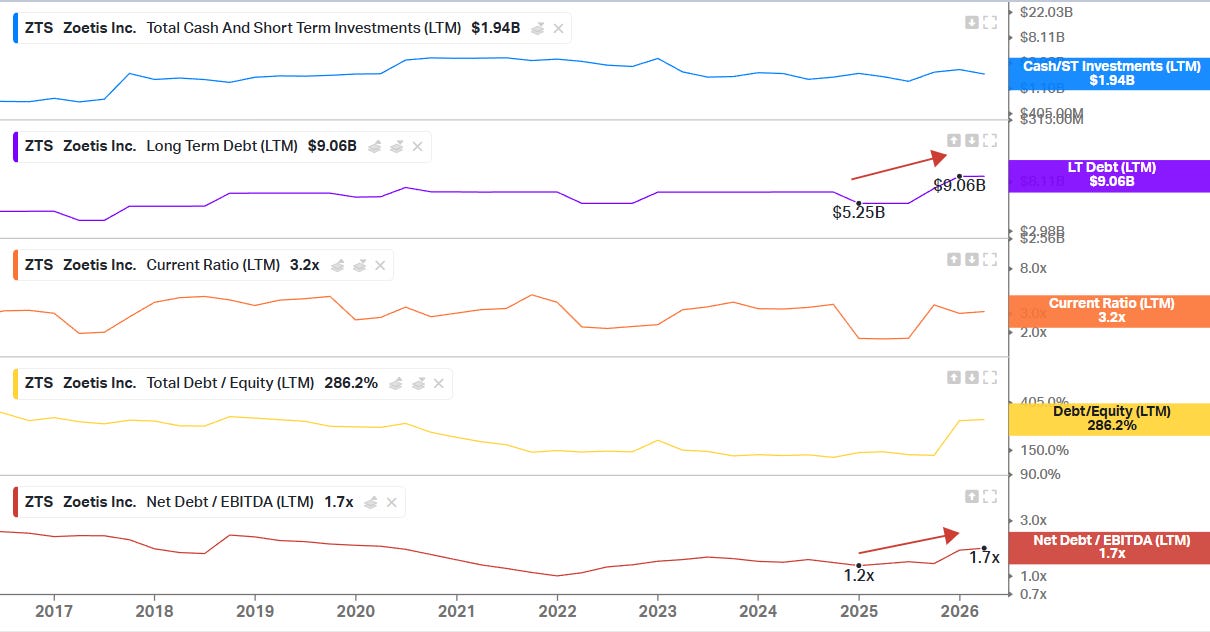

Turning to the companies financial health, ZTS has a healthy balance sheet. One metric that did stand out was the increase in debt during 2025. I’ll cover more on this later in this section.

Cash and short term investments - Zoetis has generally always had significant cash on hand. Cash is currently sitting at a healthy $1.94Bn.

Long term debt - As mentioned earlier. Debt has skyrocketed from $5.25Bn to $9.06Bn during 2025. This debt increase was a deliberate strategic choice by management to facilitate heavy share buybacks. In 2025, Zoetis spent roughly $3.24 billion on share repurchases which is a strong signal management believe the shares a highly undervalued. A total of 21.4 million shares have been repurchased representing 4.8% of the total shares outstanding.

Current ratio - a company's ability to cover its short-term liabilities (due within one year) with its short-term assets (cash, inventory, receivables) sits at a very healthy 3x.

Total debt / Equity - This has increased due to the increase in debt. However, its still at a very reasonable level of 1.7x. Also, due to Zoetis resilient earnings power I have no concern on them servicing its debt obligations.

Net Debt / Ebitda - Healthy at 1.7x. Essentially this metric tells creditors and investors how long would it take a company to pay off all its debt obligations if it used all of its earnings.

Zoetis is levered and more so recently but its backed by its strong cash generating business model. Servicing the debt doesn’t look to be a problem going forward.

D) Capital Allocation

Zoetis capital allocation strategy is prioritized as follows. Annually, the business generates roughly $2.9Bn of cash before expenditures. If your new to investing, CFO is the actual cash a company generates before capital investments.

Reinvest in the business through R&D to advance its pipeline - The company prioritizes reinvestment in its business through significant funding for research and development. This is aimed at advancing its pipeline in areas like monoclonal antibody therapies, diagnostics, and digital health. Zoetis focuses on unmet areas in animal health with a “First to market” goal.

Investments in manufacturing capacity and operation infrastructure - Investments are made to expand manufacturing facilities as demand and new products are brought to market. As you can imagine, laboratories …. and especially ones that manufacture biologics need huge investment towards high-tech bioreactors, filtration systems, and clean-room technology to meet strict regulatory quality standards.

Bolt on acquisitions - These have typically been companies in the diagnostic space as they aim to grow their presence inside veterinary’s daily workflows.

Returning excess capital to shareholders in the form of dividends and share buybacks - After the above points have been met, excess cash is then returned to shareholders in the form of dividends and buybacks. Zoetis have been growing its dividend for 12 consecutive years with a 10 Year dividend CAGR of 19.42% which currently pays out a total of $2.12 annually. At todays buy price, this equates to a dividend yield of 2.79%, way above its 10 year median of 0.64%.

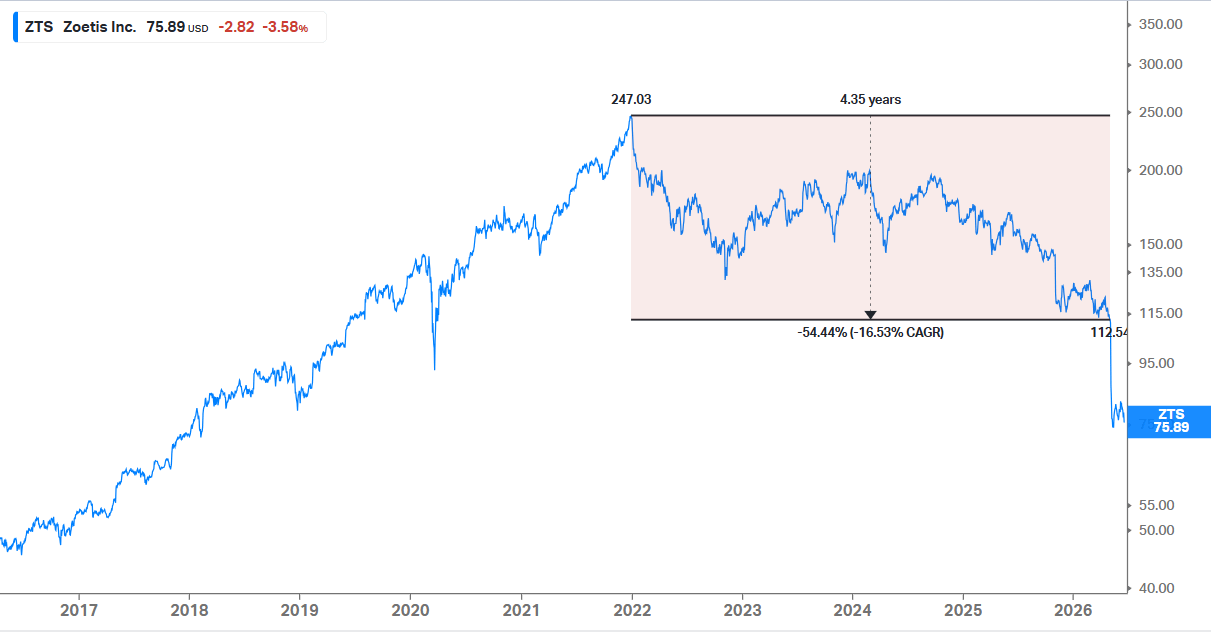

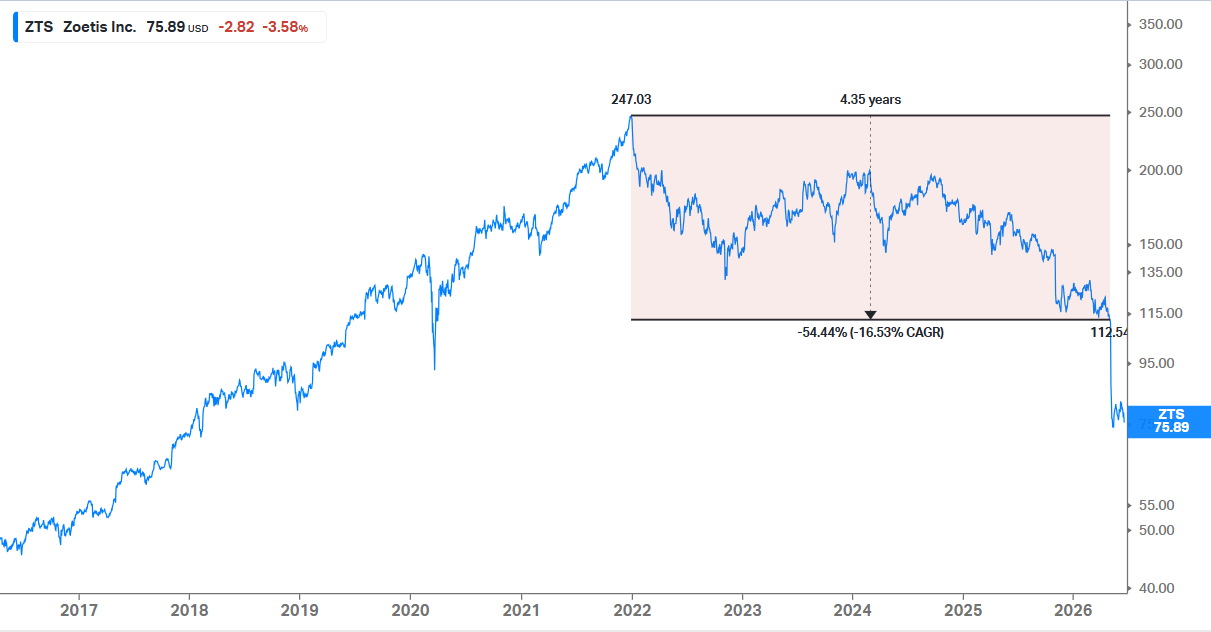

Onto buybacks. This is where in my opinion management have used financing tools to their advantage by leveraging and taking on debt to fund buybacks. During 2025, after a significant drop in share price in the region of $125, the company issued debt to repurchase a huge chunk of shares. This is an indication that management believe the shares are undervalued and although in the short term this looks like a mistake and a destruction of capital as shares continued to decline, over the long term I believe these will prove successful and be highly beneficial to EPS and FCFPS. The below chart shows the 54% share decline from its peak in 2022. Buybacks continue to be executed at these even lower prices at around $80.

E) Conclusion

Zoetis remains the undisputed leader in the global animal health sector, characterized by a highly diversified portfolio of trusted brands and geographic footprint along with a business model that historically thrives on "sticky" recurring revenues and veterinarian relationships.

Its competitive moat which is bolstered by deep-rooted relationships with veterinary clinics and a robust pipeline of high-value treatments has been challenged during 2026. The combination of persistent macroeconomic pressure on pet owners and an increasingly aggressive competitive landscape made investors question the actual durability of this moat - especially during economic downturns.

As no pipeline launches are due in 2026 - along with the headwinds they are currently facing the share price has declined dramatically and is now trading at decade low levels on a Price/FCF basis.

Zoetis is treating 2026 as a transition year and looking ahead their fate will be dependant on these two factors.

Pipeline Conversion - Can the company successfully convert its deep R&D pipeline—including promising candidates in renal disease, oncology, and chronic pain—into meaningful revenue that offsets the loss of exclusivity on legacy products?

Defending current market share - Can the company protect its market share on legacy products?

Deepening into Veterinary clinics daily workflow - Investing into their digital solutions and deepening veterinary clinics dependency on their day to day operations increases Zoetis moat and recurring revenues.

These factors are crucial on where the share price eventually leads. The "new normal" for Zoetis is a more competitive, price-sensitive environment where innovation must work harder than ever to maintain its leadership position. Their R&D pipeline is a pivotal factor here and new therapies due in 2027 and 2028 should give investors answers of where this business is heading long-term.

F) Valuation

This section will look at the possible outcomes of share price looking out into the future. I’m going to use the five factor analysis and also compare its valuation relative to the last 10 years.

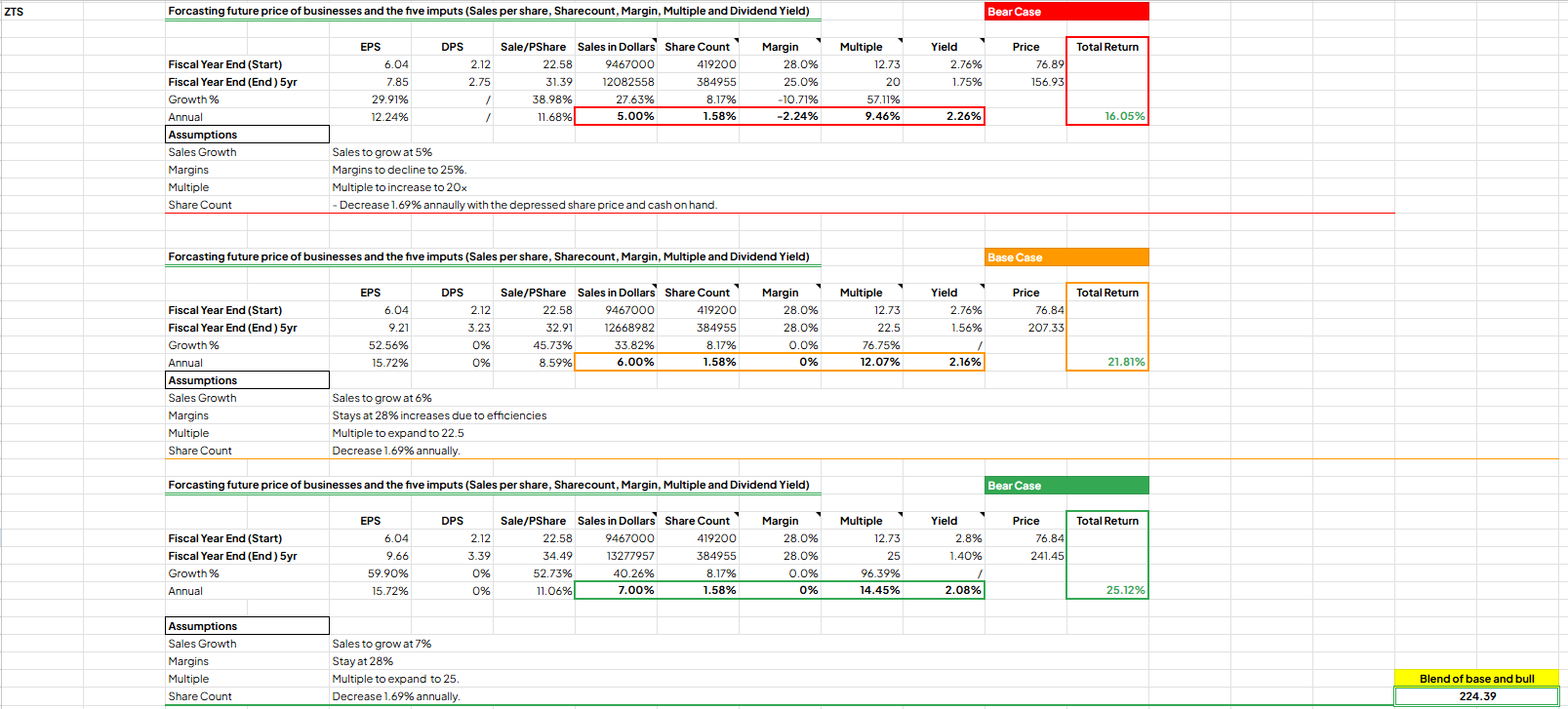

🔶Five factor analysis

The five factor analysis is my favourite IRR model and as it makes the investor see where the actual returns will coming from. It takes into account these 5 metrics.

Revenue Growth

Share Count

Margin

Multiple

Dividend Yield

Here’s my model for Zoetis ⬇️

Assumptions are relatively conservative and are by no means overly optimistic. For example in my bear case, revenue increases 5% annually, margins actually decrease to 25% from 28% today but the multiple expands to 20x. In this scenario annual returns come in at 16%. Obviously you can input any metric you feel acceptable. To achieve a blended value I use a base and bull case price and divide the two. This will give me a total IRR in the region between 21% and 25% going forward from todays prices.

🔶Relative Valuation

Below are some simple graphs looking at where Zoetis sits today relative to the past looking through a valuation lens. We can see Zoetis sits at a decade low on multiple metrics and is trading considerably lower than the companies median over the last 10 years.

However, looking at these metrics in isolation doesn’t mean much. We need to ask a few questions. Why has such a huge rerating occurred? Has the market overreacted? Can we expect the multiples to go back to historical norms?

Its clear the market is spooked by the decline in companion animal spending and the rise of generic competition. Personally, I believe the companies moat is being tested but one huge advantage Zoetis possesses is its solid relationship and deep integration into the veterinary ecosystem, trusted high quality products and their high value pipeline.

So we ask the question? Is Zoetis a broken business and in decline and is the market correct about its future prospects? Personally, I don’t think so. I see an opportunity here to own a fantastic business that’s the leader in its industry at a fantastic price.

🔶Valuation Conclusion

From my Five factor analysis model which takes into account a bear, base and bull case, I believe Zoetis offers investors very reasonable, even highly attractive IRR from todays prices. I believe I’ve been very conservative in my assumptions here which gives me some downside protection.

On a relative viewpoint, its clear to see that Zoetis is highly undervalued compared to the last decade. Obviously the the market believes its moat is being tested and its not as durable as we once thought. I can agree here to some extent. We thought that pet owners would use premium products regardless of the state of the economy. However, this doesn’t seem to be the case. Price sensitive owners are opting for cheaper generic alternatives and some are even delaying treatment which is slowing revenue growth and taking market share to lower priced competitors. Higher competition is also heating up which is another concern. However, a huge benefit is their deeply integrated business model which is rooted into Vet clinics daily workflow, developing a sticky business relationship, their first to market strategy build on a world class R&D pipeline and their trusted status for high quality products.

Zoetis is the newest addition to the DInvests portfolio.

If you’ve reached this point in the article. Thank you and I hope you enjoyed it.

Don’t forget to hit the subscribe button.

As I pointed out in January, all posts will be free to all my subscribers during 2026.

DInvests on X

I hold a beneficial position in Zoetis ZTS 0.00%↑ . My buys and sells aren’t recommendations. I can’t guarantee the accuracy of the information provided in the newsletter. All statements express personal opinions and information gathered online. Any estimates, forward looking statements and assumptions made in this newsletter are unreliable. Always do your own research. Any information in this newsletter is for educational and entertainment use only and should not be taken as investment advice.

Pawsitive Health Clinic. You asked AI to put this in didn't you? 😂