Is Pepsi a buy today?

The market hates uncertainty

Pepsi has lost over 5 years of share gains due to 11 quarters of volume declines. One huge factor investors hate is uncertainty and with these declines, its made investors question the long term growth rates and its forward valuation. In this article I will assess what returns investors can achieve purchasing Pepsi stock today.

Pepsi a global food and beverage empire.

This article isn’t intended to dive deep into the business but rather conservatively value it with a conclusion whether it will give investors a respectable return for the risk taken.

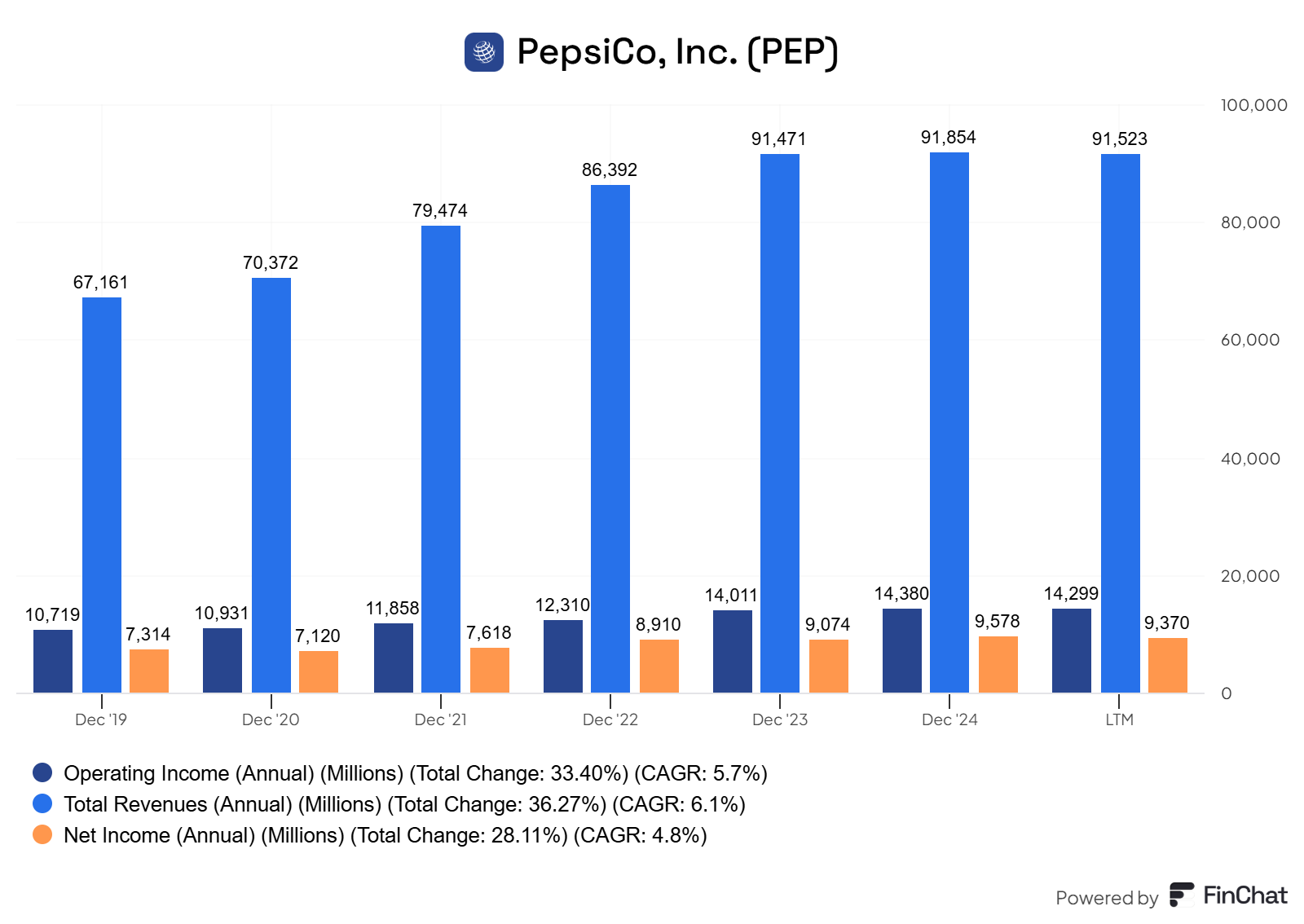

Starting from a single beverage company in 1965 then through strategic acquisitions, Pepsi has become a food and beverage empire with sales of $91.5Bn during the last twelve months. Brands such as Pepsi, Quaker & Doritos are among the worlds most favourite brands “I might be speaking on behalf of my household here” but nevertheless, there’s no doubt these brands are household names in the regions Pepsi has operations.

Below are some brands under the Pepsi unbarella.

Pepsi stock will not fit every investors criteria. Slow growth, high dividend payout, high debt and even ethical reasons might sway investors to find more suitable candidates to purchase. However, for a more conservative or solely a dividend investor, this drop in share price could give them the opportunity to add this consistent defensive stable stock into their portfolios.

Considerations

One red flag that needs to be considered is the 11 quarters of sales volumes. (Shown Below). Like any business, increased sales volumes combined with price increases contributes to healthy growth.

Will these volumes revert back to growth? That’s the key question. The market is sceptical, after all, 11 quarters of volume declines is worrying from an investors perspective. Some things to consider.

Are consumers shifting to lower price products?

Are they losing market share to competitors?

Are GLP-1 drugs the cause?

If I was to assume, I would say consumers are switching to more lower priced products and maybe GLP-1s are to blame to some extent. Market share on the other hand I believe hasn’t been lost as consumers switching to more affordable products will soon revert back once the economy improves and in turn turning volumes back to growth as they will be against easier comps.

Pepsi has pricing power. That’s a fair statement and a common quality to companies that have a brand competitive advantage. Pepsi, like many leading brands such as Coca cola, Mondelez, Kellogg’s and Kraft Heinz can all demand higher prices for their products. However, pricing power has its limits and realistically, over the long term should only match inflation. Volume growth is key for this business to get back to the respectable multiples his managed to obtain in the past.

Dividend

Currently Pepsi will give investors a starting dividend yield of 4.06% and is at its highest over the last decade. The question investors will ask and I’ve seen many discussions on this. “is it sustainable?” With over a 100% payout ratio over the LTM, its a valid question. I would like to point out that there has been negative working capital changes totalling over $1bn which as decreased FCF and when adjusting for these would have put the payout ratio lower than the 100% mark. Even after this adjustment, the payout ratio would still be on the high end of safe payout ratios with not much room for growth if free cash flow is remaining constant. With regards to the modelling for this article I will rely on this starting yield as anything else would be speculation.

Looking into the the numbers of revenues, operating income and net income its fair to say Pepsi has been a consistent grower in the mid single digit range. Free cash flow, arguably the most important metric has been stagnant with 6 of the past 8 years having a negative effect through working capital changes. (Shown below). A negative change in working capital is a negative charge against operating cash flow for the reported period and is essentially cash tied up in the business. For this reason, many capital light businesses are favoured over capital intensive ones as more cash is available to owners. Over the next few years I believe management will focus on this area especially if volumes are decreasing to take out the cash locked in WC and in turn increase cash flows.

Overall when looking into the dividend I don’t see any reason for the company to reduce it or cut it but prepared for slower dividend growth in the future. Over the last 10 years Pepsi has averaged its dividend growth at 7.5%. I don’t see this amount of growth going forward unless the company can increase its cash flows.

Growth

For modelling purposes it’s good practice to look into the past growth rates and margins to assess future assumptions.

When looking into Pepsi stock there’s a clear trend of mid single digits (Shown below). Unless Pepsi develops products in new markets within the food and beverage categories, it would be unwise to model in higher growth rates. I believe its a fair assumption for these growth rates to continue as they have in the past driven by price increases and volume increases if or when the trend reverts.

Valuation

The model below takes into account Pepsis Net Operating Profit After Taxes (NOPAT), Reinvestment rate and Operational ROIC.

Where Growth = Reinvestment rate * ROIC.

Looking into Pepsis ROIC, excluding Goodwill and Intangibles they consistently produce 35-40% ROIC. This, along with the reinvestment rate is a good proxy for NOPAT growth rates. Here, Pepsi after deducting depreciation from net capex Pepsi reinvests on average 17.24% into growth. Multiplying these two numbers results in a growth in NOPAT of 6.85%, pretty similar to the past.

Using a 10% WACC (Discount Rate) on future cash flows and deducting net debt from enterprise value produces an intrinsic equity value of $164.5 billion dollars. Dividing this into the total shares outstanding results in an intrinsic value per share of $119 dollars for Pepsi stock.

As intrinsic values are never precise and all differ to different assumptions I would say Pepsi stock is fairly valued today of $130-$135 dollars per share in my personal opinion when calculating in a 10% discount rate.

Is Pepsi stock A buy today? Conclusion

Like I mentioned at the start of this article. It all depends on the investors preference and investment strategy. From a modelling perspective a 10% return from todays prices isn’t unrealistic and very much doable. However, the risks of GLP-1 drugs, consumers shifting to lower priced products as the economy is struggling and losing market share to competitors are certainly considerations to consider.

For a passive income investor, Pepsi offers a very attractive 4+% starting yield. Also for a more conservative investor looking to preserve capital, Pepsi might be a good option for a stable defensive name in a diversified portfolio. For the growth investor, Pepsi looks like it might not offer the multi-bagger potential ones looking for.

Personally, there still isn’t enough to persuade me to pull the trigger into a position with Pepsi stock. A bigger drawdown and a higher margin of safety would make me reconsider. After all, Pepsi is a quality business with excellent brands and high ROIC.

Thankyou for reading

DInvests

DRGInvests on X

Disclaimer: I do not hold a long or short position in Pepsi stock. I can’t guarantee the accuracy of the information provided in the newsletter. All statements express personal opinions and information gathered online. Any estimates, forward looking statements and assumptions made in this newsletter are unreliable. Do your own research. Any information in this newsletter is for educational and entertainment use only and should not be taken as investment advice.

Great article and agree with your conclusion that there isn’t any catalyst for the stock to work and the valuation still seems fair. I personally prefer looking at the ingredient names in this space who despite having a higher beta/being more volatile have higher organic growth and are the true innovation engines in the food and beverage (+ fragrance and HPC) world. But for dividend investors of course those staple companies like PepsiCo are very reassuring names to own.