Estee Lauder Earnings Update : Dreadful Q1

A quick look into the quarter.

Results

Estee Lauder reported horrific earnings on 31st October 2024. A bit ironic considering the date. I will highlight what I believe to be the most important talking points.

- Net sales came in at 3.3B a decline of 4% Y/Y. The sales decline was primarily due to the continued consumer environment in Mainland China and the low conversion rate in their Asia travel retail channel which were down mid double digits Y/Y. Although management are optimistic medium-to-long-term with the new stimulus measures issued in China they anticipate short term declines in the near term.

- One positive was the increase in gross margin which expanded 3.1% Y/Y. This was achieved from better inventory management as part of their ongoing PRGP resulting is less inventory obsolescence charges. Management did guide for any benefits in gross margin will be lost with advertising to support new product launches in 2025.

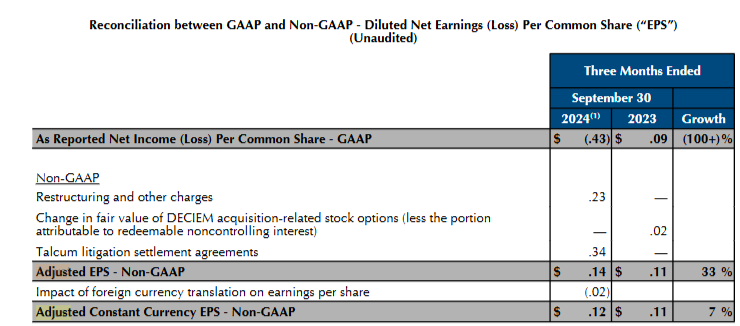

- Ebit for the company was -$121 million. This loss was due to a settlement for talcum powder cases with certain plaintiff law firms of $159 million with covers future claims over the next 5 years.

- GAAP net income was -$0.43 during the quarter. Adjusted net income (Accounting for restructuring charges and the charges from the talcum litigation, these charges totalled $0.57) came in at $0.12 in constant currency.

Dividend Cut

One huge shock to investors was the cut to the dividend by 46.9% to a quarterly dividend of $0.35 from $0.66. I have to admit, I didn’t see this coming due to the healthy balance sheet and Estee lauder in no financial distress. Was this the company sending a message to shareholders that the current operating environment will last longer than expected? I can’t think of another explanation myself. Here’s a question from one analyst during the EC

“I wanted to talk a bit about the dividend cut, both in terms of timing and kind of the message. So first, just in terms of timing, why not clean this up back in office? I know that China worsened during the quarter. But I would argue it's not to the degree that dividend should have come into question. And then the second thing is just on the message. Should we be thinking here about it because of time line and magnitude of earnings recovery when we think out over the next several years, should we be thinking about cash and reinvestment needs because there's hardly a leverage problem, there's not a balance sheet problem, but this is a pretty big change.”

Here’s Tracy Travis (CFO) response

“Look, reducing our dividend is not an indication at all of what we think about our long-term growth opportunities. Given the pressures, not only in the first quarter, which, to your point, we expected, but in the second quarter, which is a difference, obviously, than where we were in August. As we looked at recognizing the level of uncertainty that we are experiencing for the balance of the year, which caused us to pull our guidance.

We thought it appropriate at this time as well to look at the dividend. When you think about paying $0.66 dividend with the earnings, the $0.14 that we had in the quarter. And obviously, what we guided for the second quarter, it was appropriate for us to rightsize the dividend at this time to make sure. Obviously, we don't have a liquidity problem to your point, but recognizing the prolonged situation in terms of pressure in our markets, rightsizing the dividend still a very good dividend yield for investors.

But rightsizing it was the appropriate thing to do to protect the cash that will be needed, obviously, for additional actions that we may take under the PRGP as well as additional investments we may make to support growth. So really looking at it into totality in terms of total shareholder return and figuring out what's the best way for us to invest back in the business as well as obviously continue to return a nice yield in terms of dividend to our shareholders.”

We can see management are being conservative as the first half of 2025 EPS guide isn’t looking great, taking into account the guidance given for Q2 at the midpoint and EPS earned in Q1 we would have a pay out ratio of over 300%. Adding the extended uncertainty in the near future within their main markets could be the best choice, especially with the transition of the new management. Personally I would prefer this than any financial distress further on.

Outlook

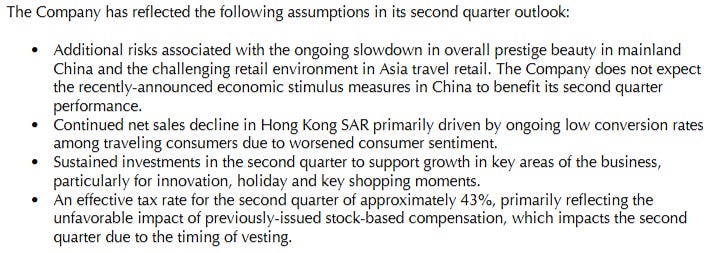

Management withdrew guidance for 2025. Again, another huge negative for the quarter and in my opinion the main driver for the huge share price plunge during the trading day.

Second Q guidance was given and it wasn’t great.

- Sales to decline -6 to -8%

- GAAP EPS between $0.02 - $0.19 (These estimates further costs related to the PRGP being dilutive of between $0.15 - $0.18

Conclusion

The drop in share price was justified in my opinion. It was a dreadful quarter and the lack of clarity given by management for the second half of 2025 was worrying. It looks like investors will have to wait until growth resumes in China and their Asia travel retail channel before any meaningful change in investor sentiment.

There’s no doubt in my mind that Estee Lauder is under earning and hopefully the PRGP plan will offset most of the declines in revenues this year to keep profitability on an adjusted basis on track. I’m not hoping for much in 2025 and I’m now looking at fiscal 2026 to start seeing a shift in revenue growth. The dividend cut was disappointing as it yielded a nice 3% and was a decent incentive waiting for a turnaround, however I can see the logic behind the decision.

On 1st January 2025, new CEO Stéphane de La Faverie will take the reigns and it will be fascinating to see what he has planned. Thanks for reading.

D Invests (DRGinvests) on X.

Disclaimer: I have a beneficial long position in Estee Lauder stock. Stocks mentioned are not investment advice. I can’t guarantee the accuracy of the information provided in the newsletter. All statements express personal opinions and information gathered online. Any estimates or forward looking statements made are unreliable. Any information in this newsletter is for educational and entertainment use only and should not be taken as investment advice.